Spectra Finance: Moving Toward a More Robust DeFi IRD Ecosystem

Spectra makes DeFi interest rates more predictable with fixed yields, tradable future yields, and better tools for managing risk.

Imagine this: You deposit 10,000 USDC into Aave at a solid 10% APY, expecting to earn 1,000 USDC in a year. But the APY drops to 5% soon after, cutting your expected earnings in half and messing up your plans.

Enter Spectra—a crypto project that fixes these problems and more. Spectra lets you lock in fixed rates for steady returns and trade yield and earn on your liquidity. These tools, often out of reach for regular traders in traditional finance, are now available to everyone.

This research report explains the basics of interest rate derivatives (IRDs), their strengths and flaws in traditional finance, and how Spectra's IRD design supercharges DeFi on Ethereum. We also dive into the technical details of the Spectra protocol and explore the future of IRDs in DeFi.

Setting the stage: Interest Rate Derivatives (IRDs) in traditional finance

Interest Rate Derivatives (IRDs) constitute a foundational element of traditional financial markets, providing instruments for managing interest rate exposure and enhancing liquidity on a global scale. These instruments—such as interest rate swaps, futures, and options—enable various market participants, including businesses, banks, and investors, to navigate the complexities of evolving interest rate environments. By locking in borrowing costs, hedging against unfavorable rate movements, and facilitating long-term strategic planning, IRDs are critical tools for achieving predictable financial outcomes.

The magnitude of the IRD market, which the Bank for International Settlements (BIS) estimates to exceed hundreds of trillions of dollars in notional value, underscores their significance. This vast liquidity contributes to ease of entry and exit, more accurate pricing, and reliable benchmark references for various financial instruments. IRDs stabilize fluctuations, ensuring unexpected interest rate variations do not fundamentally disrupt corporate operations, institutional strategies, or governmental fiscal policies.

However, despite this immense market size and importance, IRDs in traditional finance are often inaccessible to everyday traders. Complex pricing models, high entry costs, and strict regulatory requirements create barriers that typically limit participation to large institutional players and accredited investors.

Put simply, IRDs transfer exposure to future interest payments. The principle extends to instruments like government-issued Treasury bills (T-bills), which pay interest at maturity. Holding a T-bill is akin to expecting a defined return over a fixed period. An IRD, such as a futures contract on these T-bills, allows participants to trade the right to receive that future interest. For instance, if a market participant anticipates an increase in interest rates, entering into a suitable IRD position may yield profits as rates increase.

In established capital markets, IRDs facilitate complex and large-scale trading activities. Corporations employ interest rate swaps to fix borrowing costs, investors hedge bond portfolios against volatility, and banks more efficiently align assets and liabilities. Although the market structures differ from simpler examples, the underlying principle remains consistent: IRDs enable the redistribution of exposure to future interest payments, allowing for more controlled, strategic, and risk-adjusted financial operations.

From TradFi to DeFi: The evolution of IRDs

The rapid advancement of decentralized finance (DeFi) underscores the need for more sophisticated mechanisms to manage yield and interest rate risks. In contrast to traditional finance (TradFi), DeFi operates within a decentralized environment characterized by transparency, automation, and permissionless access. This setting provides fertile ground for introducing and evolving IRD-like instruments adapted to decentralized protocols.

Despite their enormous market size, IRDs have historically been difficult for regular traders to access in TradFi due to:

- Complexity: IRDs involve intricate pricing models, specialized risk assessments, and advanced market knowledge, making them challenging for non-professionals to understand and engage with.

- High barriers to entry: Trading IRDs typically requires significant capital and membership or accreditation on institutional platforms, effectively shutting out smaller or individual traders.

- Regulatory constraints: Stringent regulations often restrict participation in accredited investments or large institutions, severely limiting the ability of everyday users to benefit from IRDs in traditional markets.

- Market centralization: IRDs in TradFi are traded on centralized exchanges or over-the-counter (OTC) markets. Both approaches have limited transparency and accessibility compared to decentralized platforms.

- Cost prohibitions: Brokerage fees, complex legal agreements, and ongoing compliance costs can be insurmountable for retail participants.

Rather than simply replicating these conventional structures, DeFi protocols strive to democratize access to IRDs by leveraging:

- Permissionless innovation: Anyone with an internet connection and a crypto wallet can interact with on-chain contracts, removing the accreditation and high-capital requirements so common in TradFi.

- Automation via smart contracts: Transparent, self-executing code makes complex derivatives more approachable. This reduces the need for intermediaries.

- Composability: Often described as “Money Legos,” DeFi’s modular architecture allows IRD-like instruments to integrate seamlessly with other primitives like lending and yield protocols. This expands the utility of IRDs beyond speculation into more robust risk management strategies.

- Global accessibility: Without geographical or regulatory gating for basic usage, DeFi broadens the pool of participants who can explore, create, and trade interest rate derivatives.

A defining feature of DeFi’s architecture is its modular, composable nature. Within this framework, IRDs can function as integral components interacting effortlessly with other DeFi primitives. As the ecosystem matures and participants seek more stable, predictable instruments, IRDs are well-positioned to become essential for individual and institutional strategies, facilitating effective yield optimization and interest rate risk hedging.

This trend mirrors the evolving profile of DeFi participants, who increasingly require tools that extend beyond speculative ventures into more stable, risk-mitigated investments. IRDs meet this demand, whether serving individuals seeking to secure fixed yields or institutional portfolios managing diverse exposures.

In essence, introducing IRDs from TradFi into the DeFi ecosystem represents more than a simple technological migration. It signals a fundamental shift in managing interest rate risks within a decentralized, permissionless framework. Protocols like Spectra Finance are at the forefront of this evolution, setting a new standard for IRDs and enhancing the sophistication of yield management in DeFi’s rapidly expanding markets.

An overview of existing DeFi IRDs

As decentralized finance (DeFi) expands beyond basic token swaps and lending protocols, a diverse array of yield-bearing instruments—from lending pools to liquidity farming strategies—has emerged. This evolution has heightened the need for on-chain interest rate management tools, paving the way for decentralized IRDs.

Although DeFi IRDs are nascent, several existing platforms have introduced foundational concepts that advance yield hedging, fixed-rate investments, and broader yield optimization strategies. However, even these developments also struggle with persistent challenges that must be addressed for the sector to mature. Next, we will discuss some of these DeFi IRD protocols.

Pendle

Pendle represents one of the earlier efforts to replicate IRD-like functionality in DeFi by tokenizing future yield streams. The protocol separates underlying positions into principal and yield components, enabling the trade and speculation of future interest payouts.

Despite its widespread integration in the DeFi ecosystem, Pendle is not fully permissionless, which some argue is less aligned with the open-access ethos of blockchain. While it successfully demonstrates the conceptual viability of on-chain IRDs, the reliance on a partially permissioned architecture underscores the broader conversation around building truly trustless IRD platforms—where anyone can list new assets or create markets without centralized approval.

Notional Finance

Notional Finance takes a different approach, emphasizing fixed-rate lending and borrowing. Although not strictly IRDs in the conventional sense, these fixed-rate capabilities function similarly by allowing participants to secure predictable returns or costs. By focusing on risk management and offering longer loan maturities, Notional serves users seeking greater stability.

Nevertheless, this curated model restricts the diversity of interest-bearing markets available through the platform, limiting its capacity to serve as a comprehensive IRD solution. Participants requiring permissionless IRD creation and more dynamic trading options encounter fewer opportunities within this framework.

What are the limitations of current DeFi IRDs?

Despite incremental progress by platforms such as Pendle and Notional, several core obstacles hinder the development of a mature DeFi IRD ecosystem:

Fragmented liquidity

Existing IRD-like solutions in DeFi operate across multiple protocols, each employing distinct token standards, interfaces, and liquidity pools. This fragmentation forces market participants to navigate isolated platforms for different assets or maturities, resulting in shallow liquidity and reduced cross-asset price efficiency. The absence of a unified framework or effective aggregation mechanism also elevates switching costs and undermines the potential network effects seen in traditional IRD markets.

Permissioned infrastructure

TradiFi markets have well-established templates for introducing new IRD products. In contrast, DeFi currently lacks a widely accepted, permissionless standard for IRD creation. Existing protocols often rely on governance approvals or whitelisting processes to introduce novel instruments. This constraint restricts innovation, narrows the range of tradable assets, and prevents the ecosystem from adapting rapidly to evolving market conditions and interest rate environments.

Lack of standardization

The absence of common standards is a significant barrier to interoperability and scalability in DeFi IRDs. Unlike established traditional IRD markets governed by clearly defined contract specifications, DeFi protocols rely on heterogeneous tokenization techniques, yield-bearing token interfaces, and contract architectures.

This patchwork structure impedes seamless integration with other DeFi primitives, such as lending platforms, decentralized exchanges (DEXs), and yield aggregators. Without consistent standards, the envisioned “money lego” paradigm—where IRDs act as composable building blocks—is not fully realized.

Spectra Finance: Redefining DeFi IRDs

Addressing liquidity fragmentation, establishing permissionless frameworks for IRD creation, and pursuing standardization are critical steps in the evolution of on-chain IRDs. By implementing these improvements, DeFi can unlock a range of sophisticated interest rate management strategies currently unattainable at scale.

Overcoming these challenges would enable deeper liquidity, broader participation, and more efficient price discovery, ultimately bringing DeFi IRDs closer to the maturity, diversity, and operational efficiency of traditional interest rate markets. It could increase the utility of DeFi and make the sector more attractive to mainstream participants.

Spectra Finance represents a significant advancement in managing decentralized IRDs. By combining a permissionless framework for IRD creation, adherence to standardized token interfaces, and an inherently composable architecture, Spectra reduces complexity and broadens access. The result is a more dynamic environment where diverse market participants can engage with IRDs for hedging, yield optimization, and product innovation.

Unpacking Spectra’s value proposition

The Spectra protocol offers features and benefits that differentiate it from existing DeFi IRD solutions. We analyze these features in subsequent sections:

Permissionless IRD pool creation

Spectra is wholly permissionless, unlike many DeFi interest rate protocols that limit market formation or require permissioned onboarding. Any participant can deploy a liquidity pool to power yield swaps —all without lengthy governance approvals or centralized gatekeepers. This open-access model fosters a vibrant ecosystem of IRD markets across diverse maturities, assets, and risk profiles, giving users the flexibility to express views on future interest rates, hedge against yield volatility, or design bespoke fixed-income products.

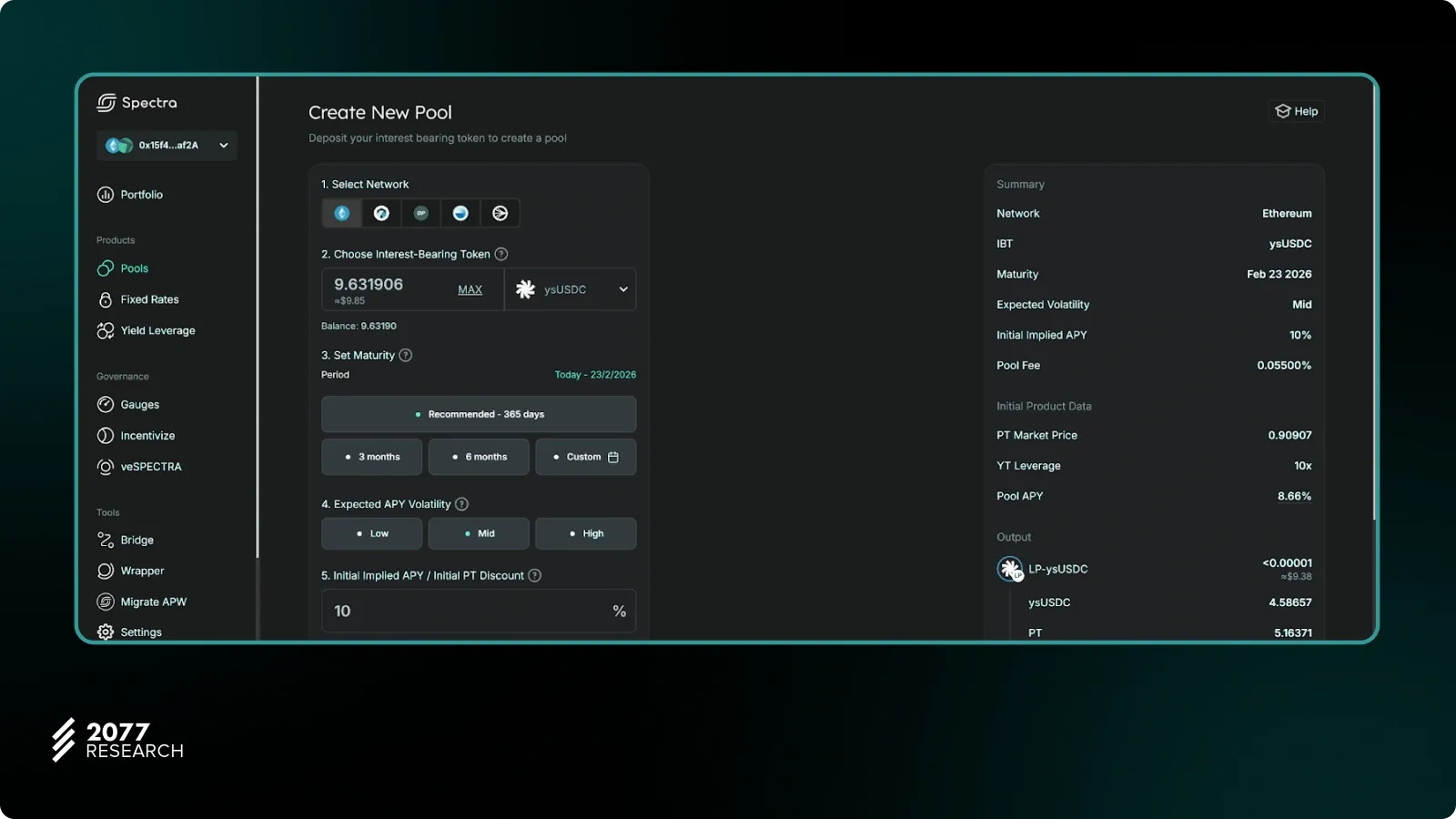

To streamline this process, the Spectra App offers a user-friendly interface requiring no specialized tools or extensive technical expertise. By selecting a compatible interest-bearing token (IBT)—such as aUSDC—and specifying parameters like maturity, expected APY volatility, and initial PT discount, users can seamlessly launch new IRD markets in just a few clicks. This approach broadens participation in both yield speculation and fixed-rate strategies, making pool creation and liquidity provisioning accessible to anyone with an internet connection.

Fixed-rate positions and yield leverage simplified

Complex yield tokenization processes are distilled into intuitive steps. Establishing a fixed-rate position resembles purchasing a zero-coupon bond, where users allocate principal, choose a maturity date, and receive a clear indication of the expected redemption value. Similarly, setting up yield leverage is no more complicated than a standard token swap. Real-time interest rate data and visualizations inform decision-making, removing the need for specialized knowledge of derivative pricing models.

ERC-4626 Standardization for interest-bearing tokens

Spectra’s reliance on underlying IBTs that follow the ERC-4626 standard is a key factor enabling its broad interoperability. Introduced in 2022, ERC-4626 provides a uniform interface for deposits, withdrawals, and accounting. This structure resembles how ERC-20 became the go-to standard for fungible tokens.

By defining consistent methods for interacting with vaults, ERC-4626 significantly lowers integration hurdles for projects that want to tokenize yield. This strategy encourages a thriving ecosystem of yield-bearing protocols, such as Frax Finance, Aave, Morpho, Yearn Finance, and Balancer, implementing ERC-4626-based vaults.

By building on top of ERC-4626-compliant assets, Spectra ensures its foundational layer incorporates widely accepted best practices in yield generation and asset management. This approach significantly reduces integration overhead, allowing Spectra to support various existing and future yield-bearing protocols.

Fully composable yield tokenization and trading

Spectra’s architectural philosophy emphasizes composability. Yield tokenization—the process of separating principal from future yield—unlocks a range of strategic opportunities that can be combined with other DeFi primitives. Beyond lending, borrowing, and automated yield-farming, Spectra’s Principal Tokens (PTs) can also underpin discounted token offerings or custom savings programs, enabling any project to build specialized financial products using the Spectra stack.

By integrating PTs into existing DeFi protocols, developers can create products and instruments that would be impossible to replicate in traditional finance. This open-ended design lowers entry barriers for IRD participation and encourages continuous innovation, as projects and individuals can experiment with on-chain interest rate derivatives cost-effectively and permissionlessly. By positioning IRDs as a “plug-and-play” component within the broader DeFi “money Lego” framework, Spectra paves the way for a wide range of customizable interest rate solutions that anyone with an internet connection can leverage.

User-friendly app and interface

While Spectra’s permissionless pools, ERC-4626 compatibility, and yield tokenization form a robust technical foundation, the protocol’s intuitive application interface bridges the gap between complexity and accessibility. Designed for both seasoned DeFi participants and newcomers exploring IRDs, the Spectra App provides familiar workflows that mirror standard DeFi interactions, thereby reducing the technical barriers often associated with interest rate derivative markets.

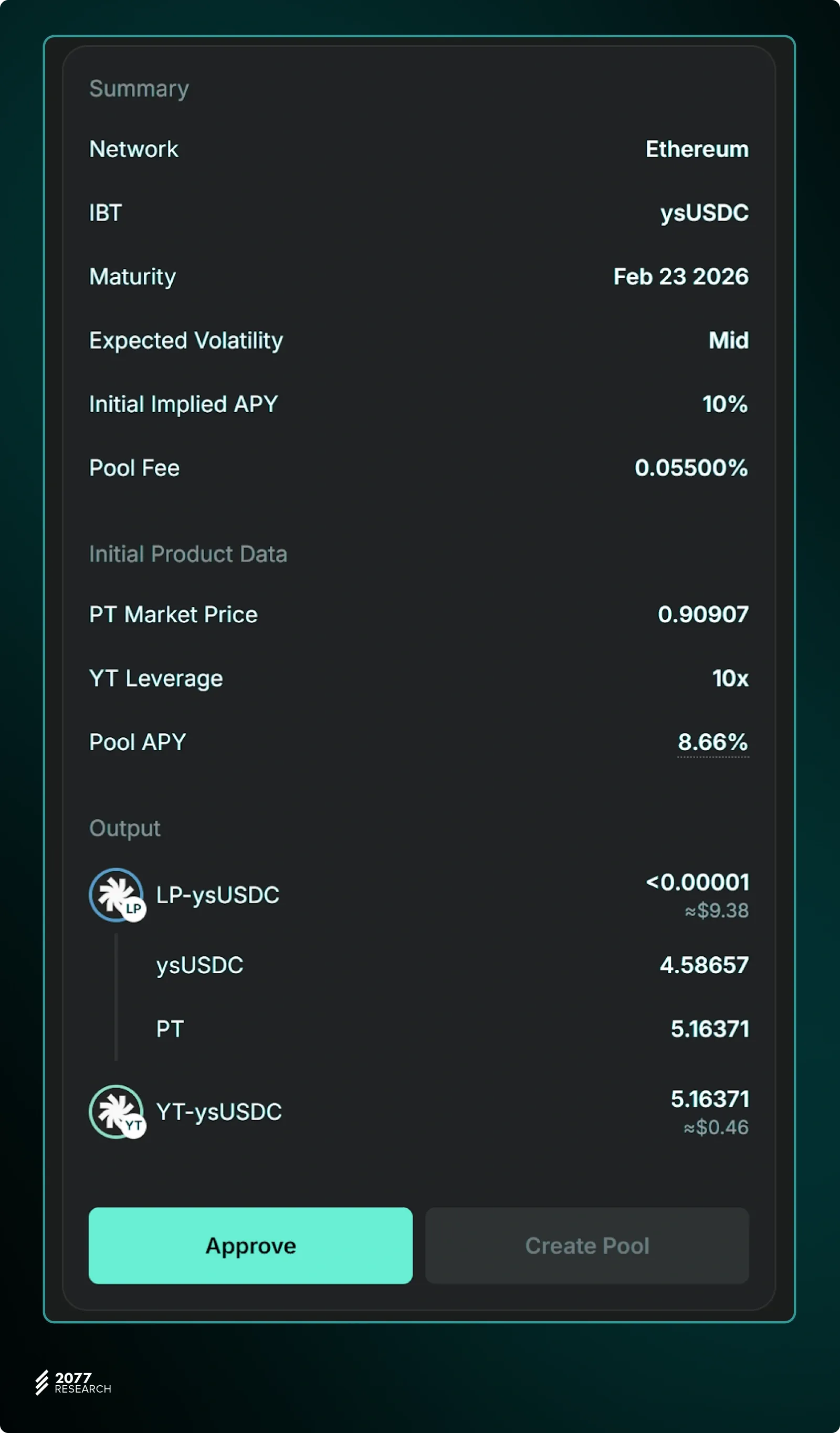

The “Create New Pool” interface, where users select a compatible IBT (e.g., ysUSDC), choose a maturity period and specify the target APY:

After selecting parameters, the interface displays the pool summary, including the resulting LP token and Yield Token:

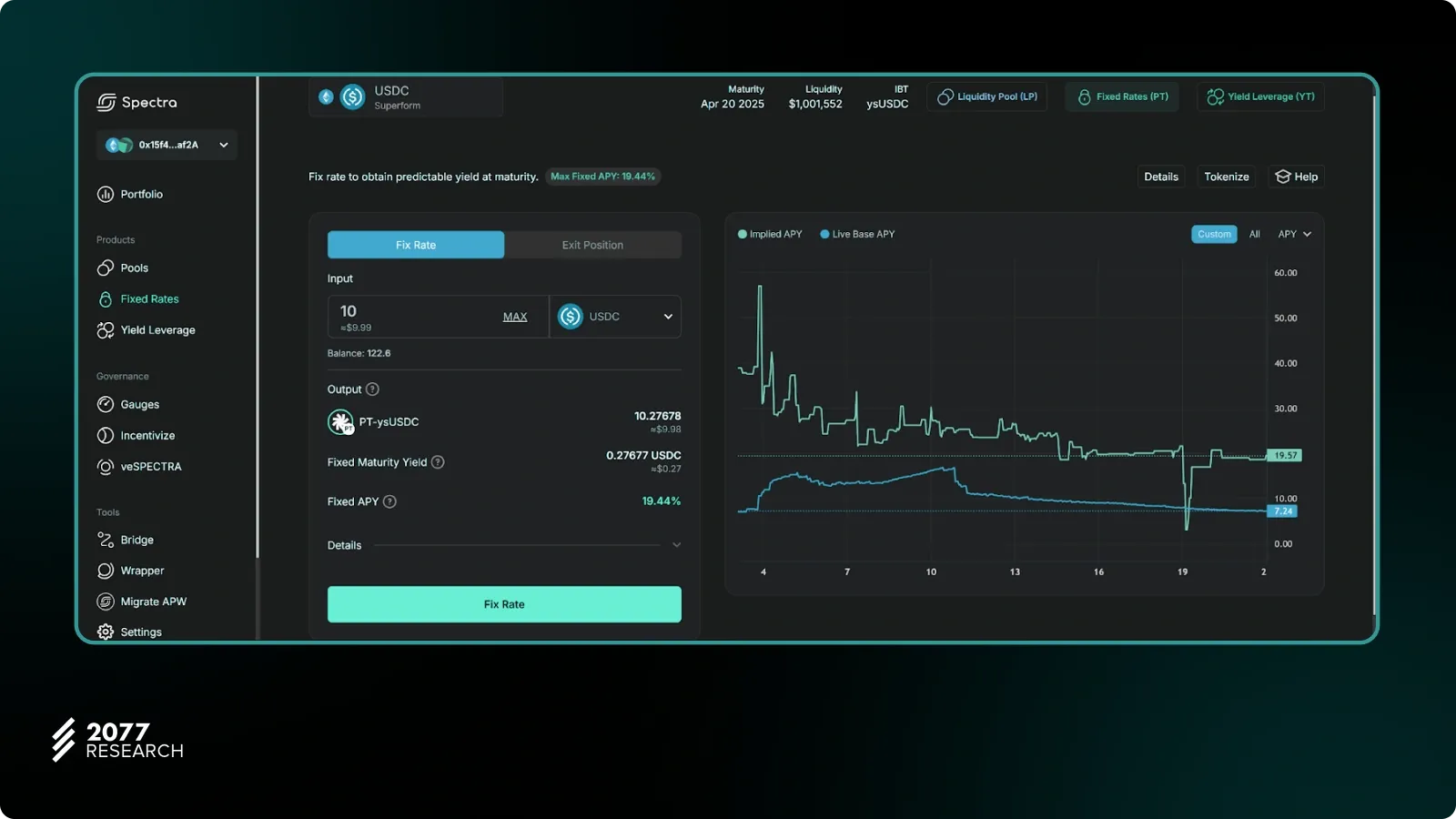

In the “Fixed Rates” panel, users convert tokens (e.g., USDC or ysUSDC) into Principal Tokens to lock in a stable APY until maturity. The top area shows details such as the maturity date and pool liquidity. After specifying an amount, the interface displays the resulting PT-ysUSDC, Fixed APY, and Fixed Maturity Yield:

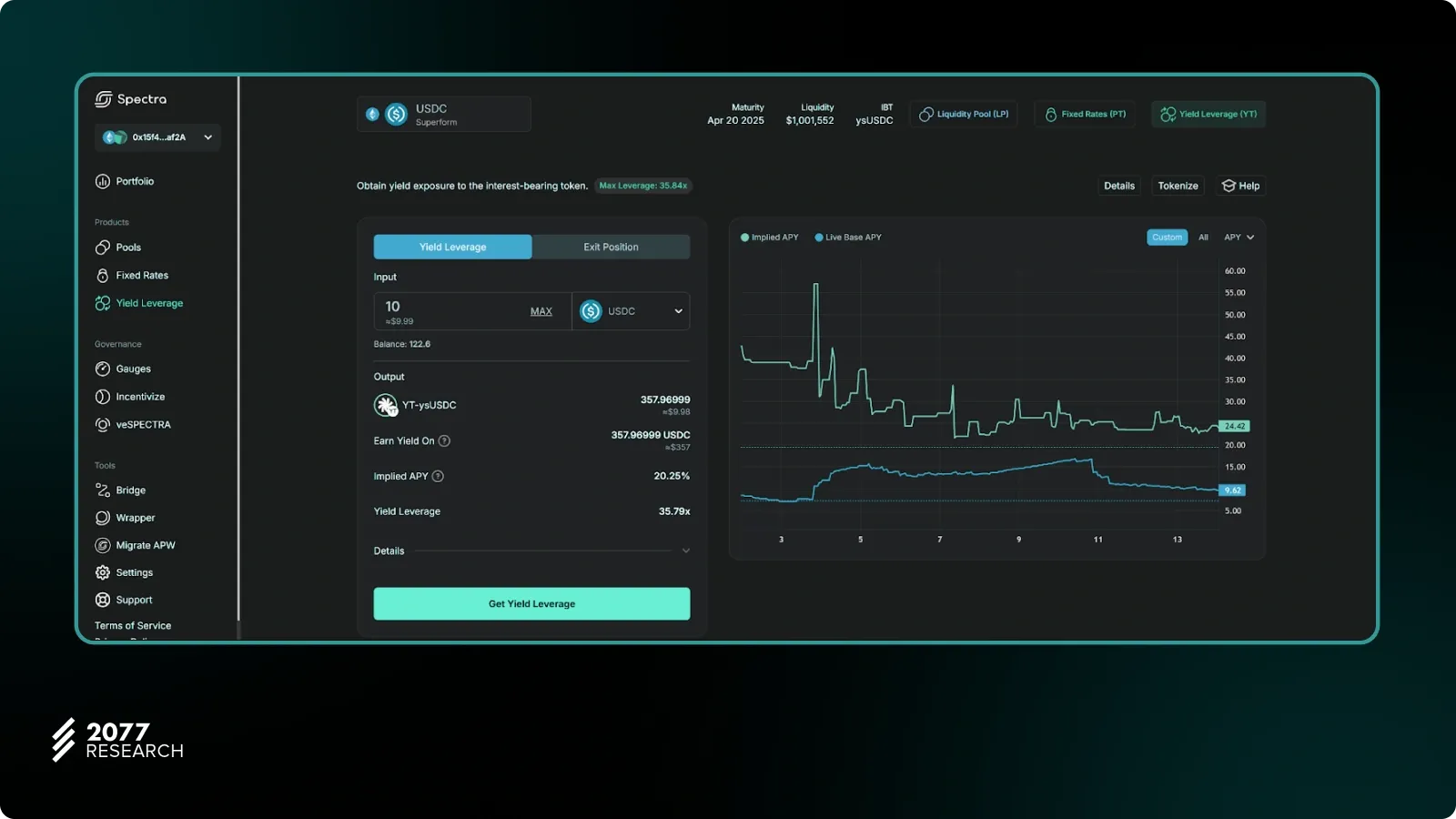

Users can buy or sell Yield Tokens to gain or reduce exposure to the floating rate of the interest-bearing token. After providing the trade parameters, the interface displays the number of YT-ysUSDC tokens the user will receive, as well as implied APY and yield leverage:

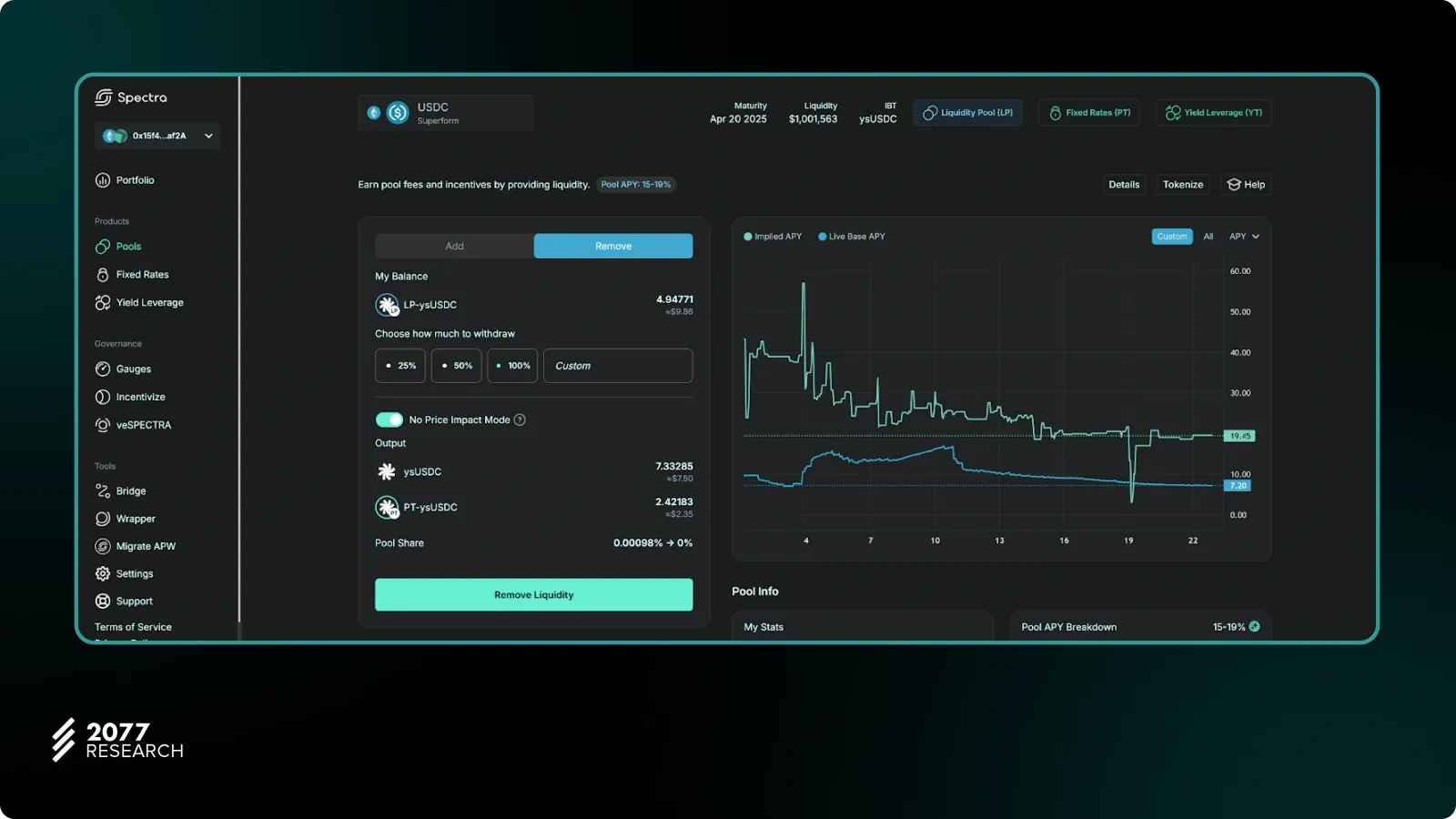

Note: Implied APY reflects the market’s current expectation of the underlying yield. It can deviate from the live IBT APY if trading volume is low and the market hasn’t had sufficient activity to converge on the actual rate or if participants factor in additional incentives—such as an anticipated airdrop—driving the implied rate higher than the base yield. Implied APY changes with every trade inside the pool.

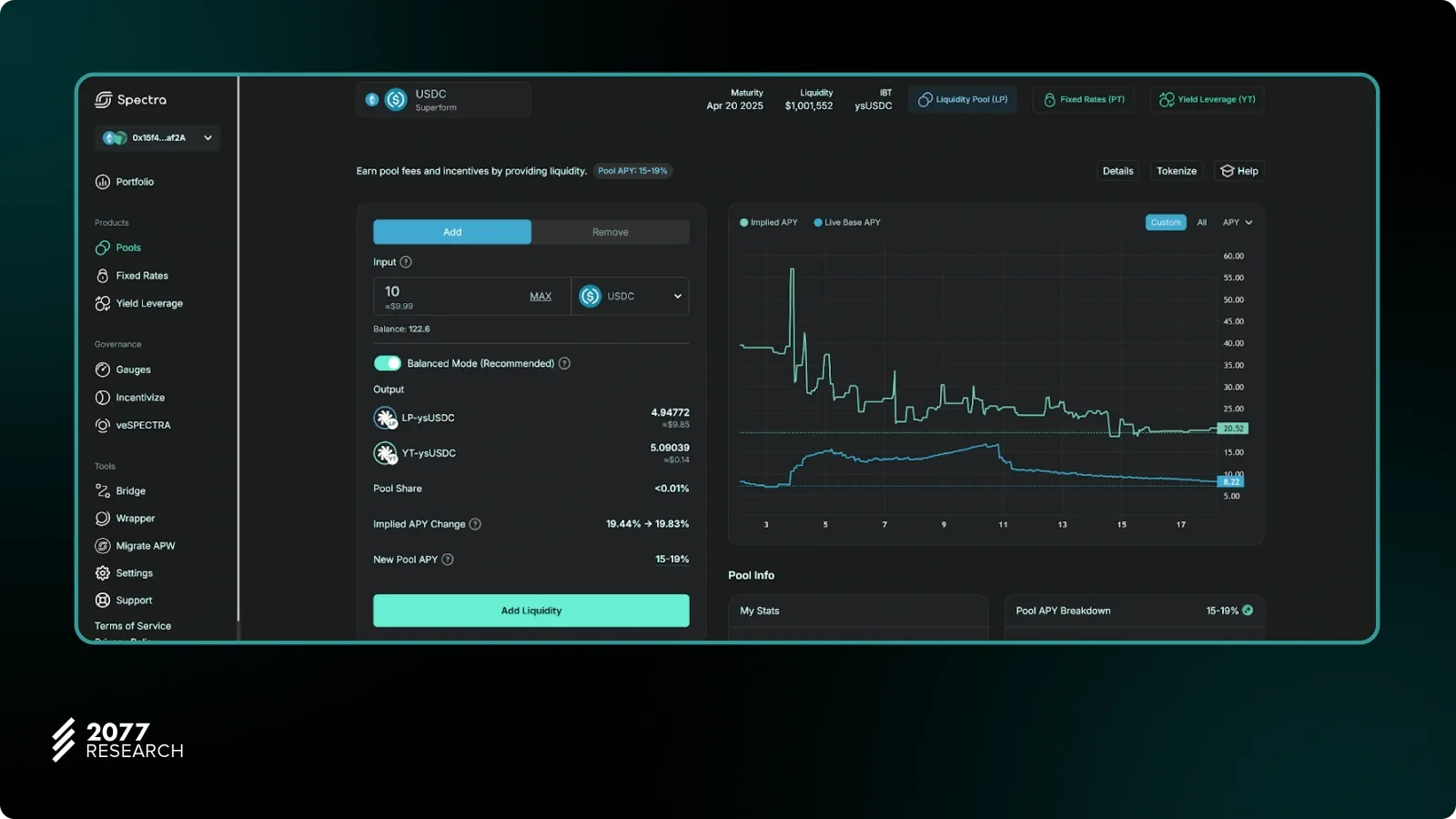

In this module, users specify the deposit amount, and the interface displays the resulting LP token and Yield Token:

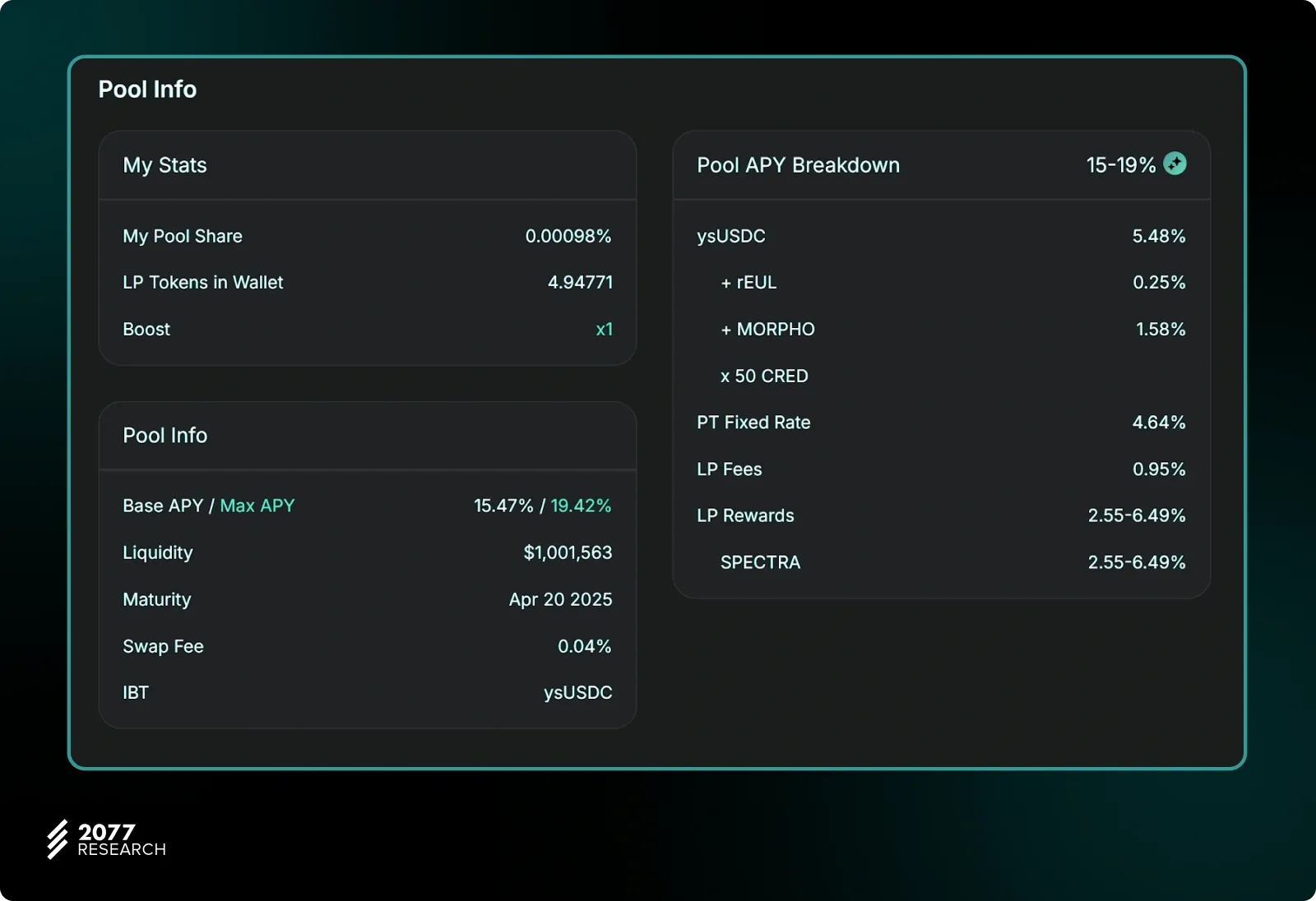

Below the APY chart, Pool Info lists key details, including the pool’s expiry date and total liquidity:

In this module, users specify the withdrawal amount, and the interface displays the resulting IBT token and Principal Token:

By combining permissionless innovation, standardized token interfaces, and a user-centric application layer, Spectra sets a new benchmark for managing IRDs within DeFi. It removes technical friction, consolidates access to diverse IRD markets, and equips participants with the analytical tools necessary for informed decision-making. In doing so, Spectra simplifies IRD engagement and accelerates the maturity of IRDs into a core pillar of the decentralized financial ecosystem.

A deep dive into Spectra’s protocol primitives

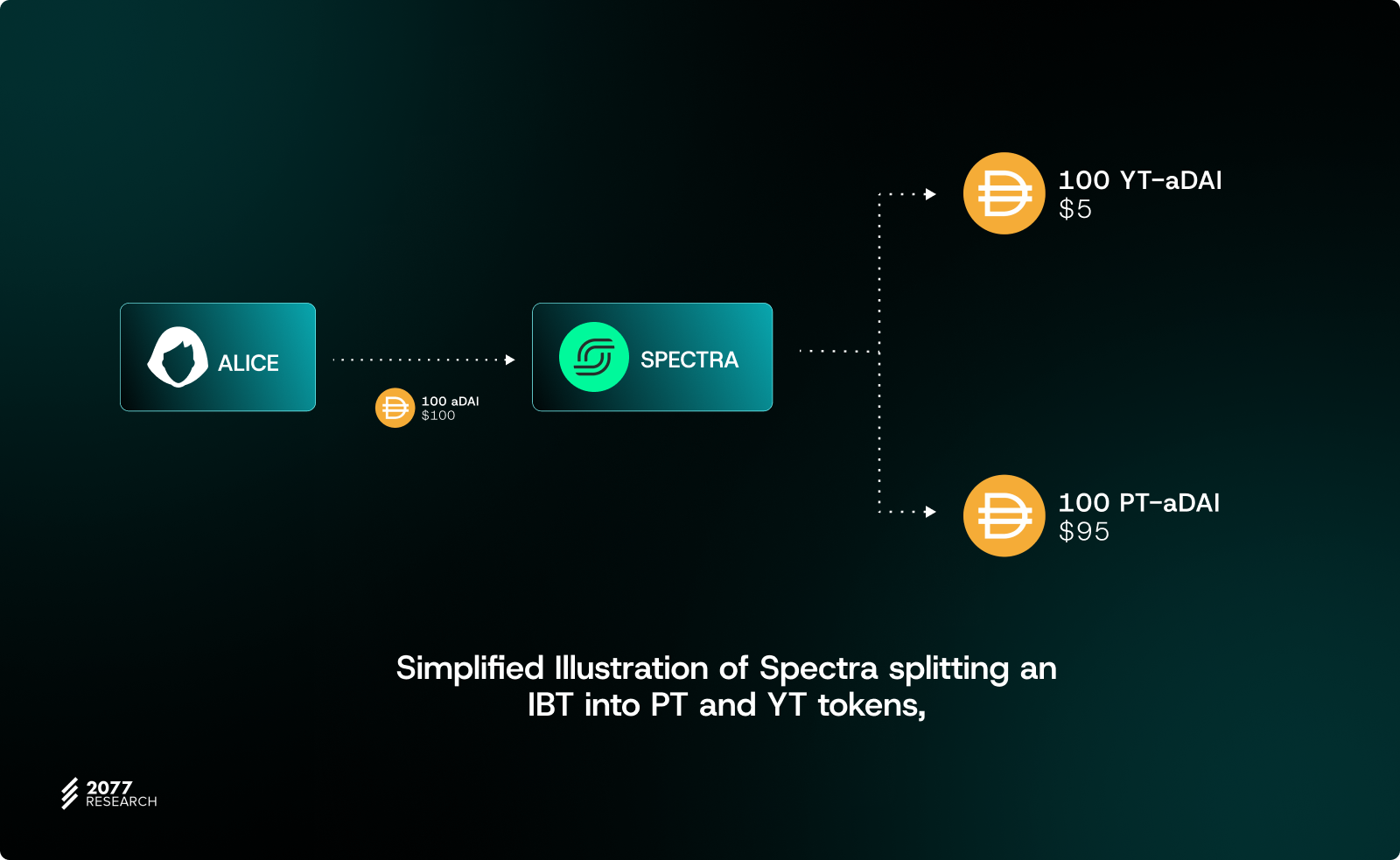

Spectra’s protocol introduces two fundamental token types—Principal Tokens (PTs) and Yield Tokens (YTs), which represent distinct components of an interest-bearing token’s value. When an ERC-4626-compatible IBT is deposited, Spectra splits it into principal and yield components.

This separation allows participants to engage with fixed-rate instruments (PTs) and yield speculation (YTs) within the DeFi ecosystem. PTs can be traded at any time and redeemed at maturity for a known amount of the underlying asset. In contrast, YTs can be traded before maturity and capture the variable interest accrued over time. Once the maturity date is reached, YTs expire, meaning they no longer earn any interest.

Principal Tokens (PTs): Fixed-rate instruments in DeFi

In TradiFi, fixed-rate bonds or certificates of deposit assure investors a predictable return regardless of market volatility. Principal Tokens emulate this concept on-chain, offering a reliable maturity-based payout that parallels the certainty of fixed-income assets. Each PT represents a future-dated claim on the underlying asset, functioning similarly to a zero-coupon bond. At maturity, holders can redeem PTs 1:1 (minus any negative yield adjustments) for the underlying asset, effectively locking in a known redemption value.

Use cases for Principal Tokens (PTs) in DeFi

- Long-term savings: PTs enable users to lock in a known return at maturity, providing stable, predictable outcomes. Rather than continuously monitoring fluctuating APYs, participants can hold PTs to meet long-term financial goals more confidently.

- Predictability in yield farming: By obtaining PTs, yield farmers secure a baseline return. While the YTs can be traded separately, the PT ensures a portion of the portfolio is insulated from adverse interest rate swings, aiding in more robust scenario planning and risk management.

- Stable collateral in DeFi lending: Lending markets (e.g., Morpho and PWN DAO) have begun exploring PT-based collateral. By offering a more predictable collateral value than the fluctuating yields of IBTs, PTs could eventually streamline lending strategies, support leverage, and foster structured products built on a more stable foundation. As protocols evolve—particularly those integrated with the Spectra ecosystem—this inherent stability may unlock new pathways for DeFi borrowers and lenders alike.

How do PTs work under the hood?

- Standards and compatibility: PTs comply with EIP-5095, representing a future claim on underlying assets, and use EIP-2612 for gasless approvals. They operate alongside ERC-4626 IBTs, ensuring broad composability and integration with other DeFi protocols and vaults.

- Deposit process: Users deposit IBTs into the Spectra protocol, receiving PTs and YTs in return. Deposits must occur before the PT’s maturity date.

- Redemption mechanics: (a) Before maturity: PTs and YTs must be redeemed together to unwind the position back into underlying assets. Both tokens are required because the yield portion must be settled. (b) After maturity: Once the PT reaches maturity, it can be redeemed independently for a predetermined amount of the underlying asset. At this point, the fixed-rate commitment is fully realized.

- Predictable yield accounting: The protocol tracks the IBT’s underlying rate, ensuring that by maturity, the PT holder’s entitlement is accurately calculated. PT holders rely on this final redemption for their fixed, predictable payout.

- Integration points: PTs’ standardized interfaces enable straightforward integration into lending platforms, automated yield strategies, and liquidity pools. Their predictable nature makes them suitable building blocks for fixed-rate financial products atop an underlying variable rate.

YTs: Speculative instruments on future yield

YTs represent the future yield portion of an IBT. Whereas PTs guarantee a fixed redemption amount at maturity, YTs track the changing interest that accrues over time. Their value depends on actualized APYs: YT token holders benefit by claiming more yield than initially expected if rates rise. YT holders can claim accrued yield at any point before maturity.

Use cases for YTs

- Interest rate speculation: Traders expecting rising interest rates can accumulate YTs to benefit from higher-than-expected yields. As the interest-bearing token’s live APY rises, its respective YT holders gain a proportionally larger share of the yield, effectively turning favorable interest rate shifts into profits and providing an avenue for interest rate speculation.

- Layered yield strategies and incentive programs: Participants can incorporate YTs into specialized yield-farming or reward mechanisms. For instance, some protocols may offer additional staking options or reward programs specifically for YT holders—whether through extra governance tokens, loyalty points, or bonus yields. By isolating the yield portion of an asset, YTs enable creative financial products that focus on fluctuating interest returns, allowing users to pursue more nuanced strategies.

- Airdrop speculation: In certain protocols, IBT holders may be eligible for airdrops or additional rewards. It is important to note that the key reason users purchase YTs is because it gives them the biggest exposure to airdrop per $1 spent, thanks to its Yield leverage feature. Yield Leverage refers to notional exposure or the yield-generating power you get per dollar spent. If Yield Leverage = 91.66x, this means that for every $1 spent, you get $91.66 worth of the underlying interest-bearing asset.

- Once an IBT is split into Principal Tokens (PTs) and Yield Tokens (YTs), the yield (including airdrop eligibility) effectively flows to YT holders. Because YTs cost less than acquiring the full IBT position, speculators gain a higher notional exposure (known as “yield leverage”) for each dollar spent—thus securing a larger share of airdrop. If an airdrop is later announced, YT holders enjoy maximized benefits relative to their initial cost. While the YT’s market price may also appreciate, the primary draw is this elevated exposure per dollar, enabling speculators to capitalize on potential distributions more efficiently than by holding the entire IBT outright.

How do YTs work under the hood?

- Redemption mechanics before expiry: Before the PT’s maturity, YTs function like standard ERC-20 tokens that track and distribute yield of its corresponding interest-bearing token. Because they represent a claim on variable interest, YT tokens can be freely transferred, traded, or held while the underlying IBT’s rates fluctuate. The timing of yield distribution depends on the design of the underlying IBT; some tokens, such as Aave’s aUSDC, accrue yield continuously (e.g., per block), while others might distribute yield at fixed intervals (e.g., daily or weekly).

- Redemption mechanics after expiry: Once the PT’s maturity date is reached, YTs no longer represent any future yield. Their value effectively becomes zero, reflecting that all yields have been fully allocated or redeemed. To maintain clarity and prevent misuse, transfers of YTs are halted after maturity, ensuring no state-changing actions occur once the yield-bearing lifecycle has ended.

In essence, YTs represent a dynamic, tradable claim on future yield until it expires. After expiry, they effectively revert to zero-value tokens, and the token design prohibits any transfer attempt. A curious reader can check the Technical Appendix: Yield Token Implementation at the end of this article for a detailed explanation of what happens to YT tokens after the maturity date.

Automated Market Maker (AMM) Pools

Spectra’s protocol design enables the permissionless creation of AMM pools for trading PTs and YTs. Rather than relying on a proprietary AMM, Spectra is AMM-agnostic, meaning it can integrate with various external liquidity infrastructures.

It is leveraging the Curve AMM due to Curve’s proven reliability and well-understood behavior. Pool creators are responsible for setting appropriate parameters, such as the curve’s shape, to minimize impermanent loss and maintain efficient pricing. When creating a pool on Spectra’s interface, users choose the expected APY volatility from low, mid, or high. This strategy ensures that pool parameters are adjusted according to the volatility of the associated interest-bearing token. However, more sophisticated users can customize their own parameters by using the deployCurvePool() function. Spectra’s developer documentation provides guidelines for parameter choices to improve long-term pool stability.

PT-IBT pools

The liquidity mechanism in Spectra pairs Principal Tokens (PTs) with their corresponding Interest-Bearing Tokens (IBTs) in PT/IBT pools. These pools allow traders to buy and sell PTs efficiently while earning swap fees to liquidity providers (LPs).

In contrast, creating AMM pools directly with YTs poses practical challenges. Since YTs become non-transferable after maturity, liquidity providers would have to exit positions prematurely as maturity approaches, potentially increasing volatility and reducing overall market efficiency near the end of the yield period.

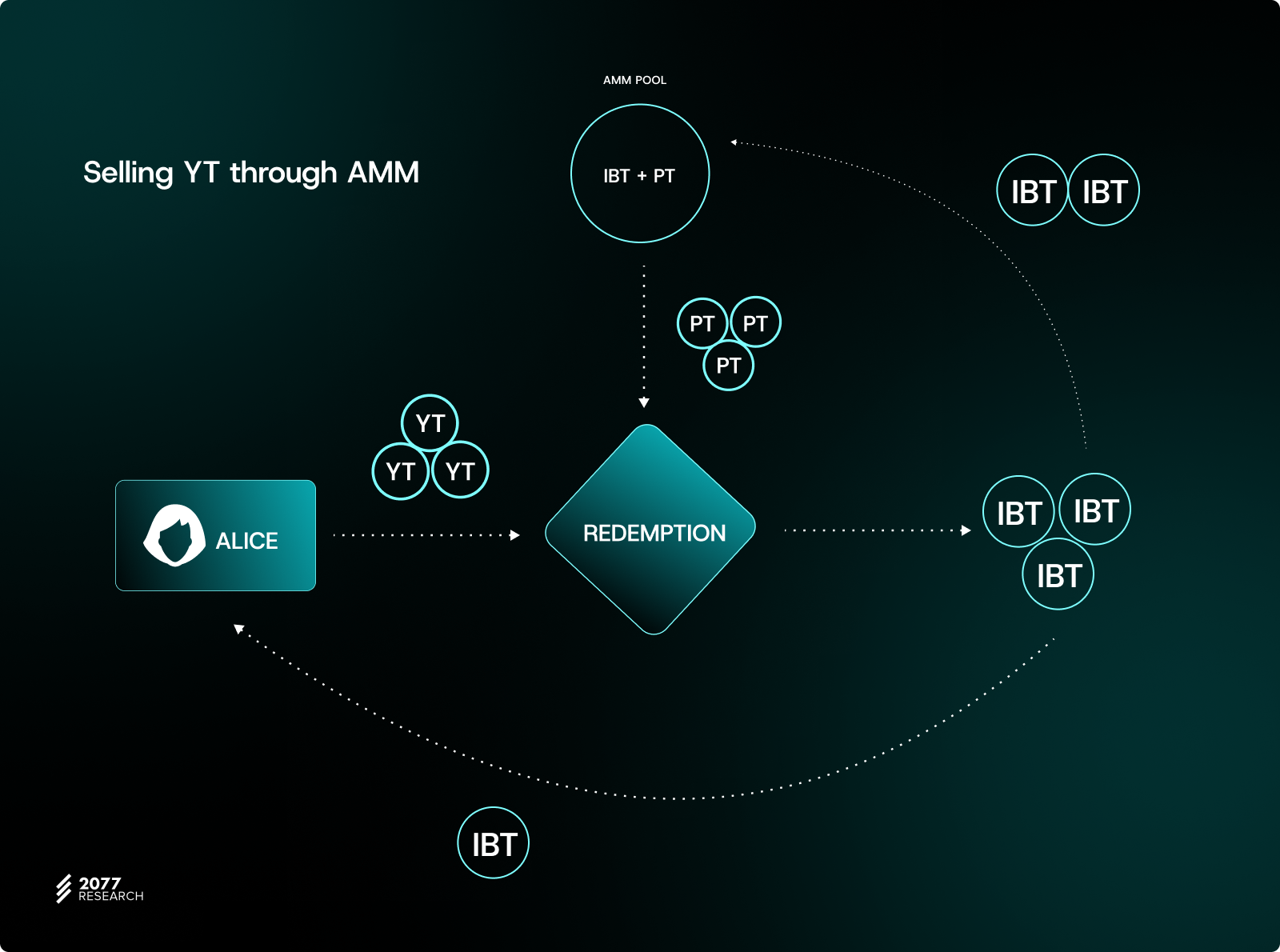

Instead of establishing direct YT pools, Spectra employs a flash swap mechanism, using the PT-IBT pool as a liquidity source. Consider a scenario where the user, Alice, wants to sell YTs.

Upon her transaction, the protocol initiates a flash swap from the corresponding PT-IBT pool, borrowing a matching amount of PTs. The underlying principal asset is redeemed by combining these borrowed PTs with Alice’s YTs. The protocol then provides Alice with the corresponding principal asset and returns any remaining assets to the pool.

The flash swap mechanism lets users sell YTs into interest-bearing tokens via the PT-IBT pool

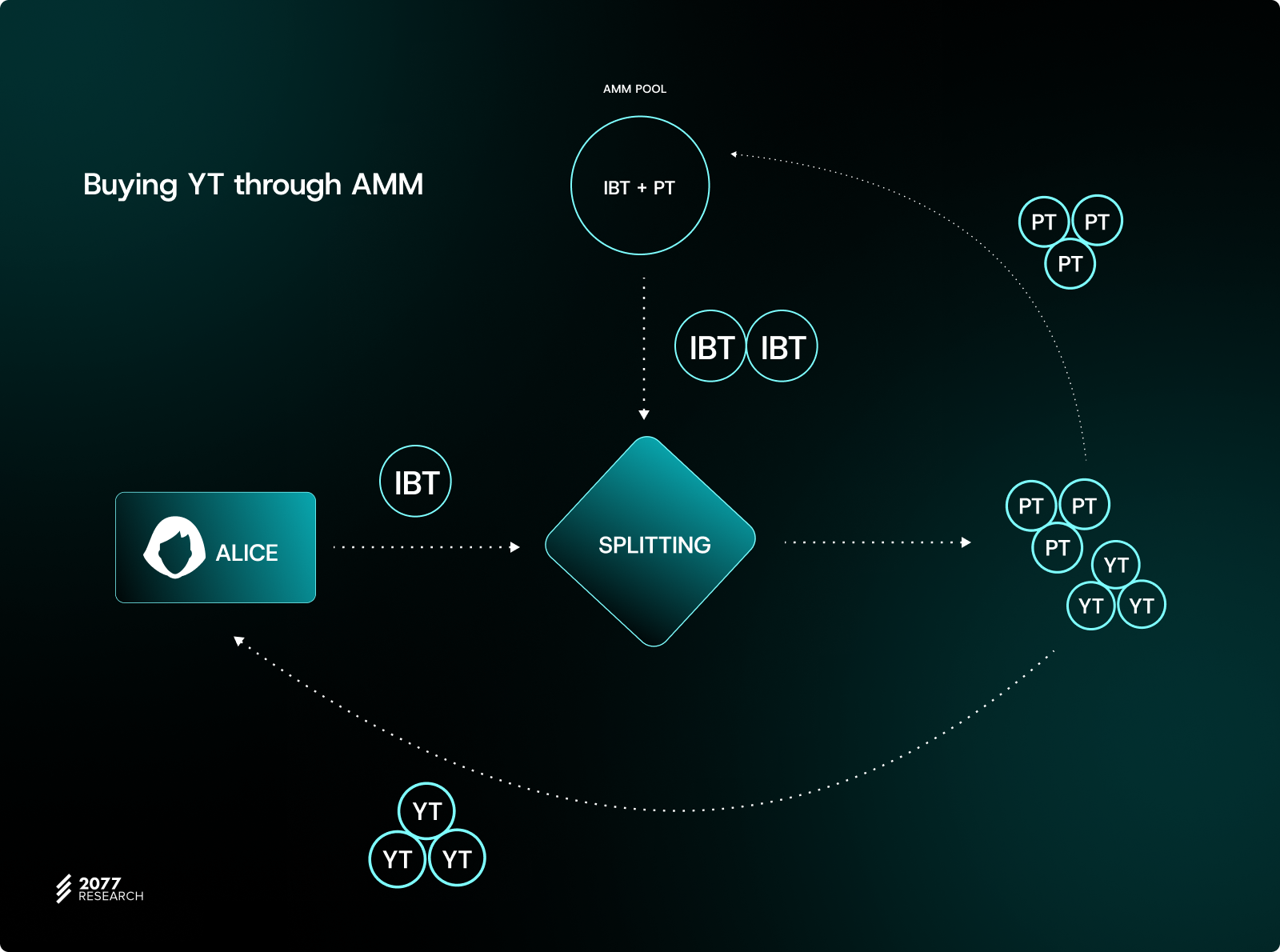

A similar process occurs when Alice wants to buy YT tokens: the principal assets in the pool are utilized to create YTs, which are delivered to Alice, while PTs flow back into the pool. This approach allows users to trade YTs indirectly without requiring a dedicated YT-asset pool and prevents complications related to YT’s post-expiry restrictions.

The flash swap from the PT-IBT pool enables YT purchases without separate YT liquidity

Price dynamics and arbitrage

The price relationship between PTs, YTs, and the underlying principal asset is critical to maintaining stable markets. The principal asset’s price can be considered the sum of the PT and YT prices.

Arbitrageurs play a key role in enforcing this relationship because where the principal asset’s price falls below the combined value of the PT and YT, arbitrageurs profit by acquiring the principal asset and splitting it into PT and YT tokens for resale.

Conversely, if the principal asset’s price is higher than the sum of PT and YT, they can combine PT and YT to redeem the principal asset and capture the price difference. This continuous arbitrage activity ensures that PT and YT valuations remain consistent with underlying fundamentals.

Implications for fixed yield and market depth

Since PT prices move in tandem with changes in YT values, the effective “fixed yield” for a PT holder comes from the price difference between the principal asset and the YT component. AMMs, by their nature, price assets as a function of swap size, meaning that large trades can shift prices and impact yields.

Consequently, participants must consider trade size and available liquidity when evaluating PT and YT valuations and the resulting effective yield. As liquidity deepens and markets mature, pricing dynamics stabilize, supporting healthier interest rate derivative markets within the Spectra ecosystem.

ERC-4626 integrations

Understanding IBT Types: Rebasing vs. non-rebasing

IBTs can be categorized as either rebasing or non-rebasing assets:

- Rebasing IBTs: These tokens periodically adjust user balances to reflect accrued yield. Instead of the token’s value increasing, each user's total number of tokens grows proportionally over time. Most rebasing tokens comply with the ERC-20 standard, but their total supply and individual balances are regularly updated to “rebase” the token count.

- Non-rebasing IBTs: Non-rebasing tokens maintain a fixed number of tokens per user. As yield accumulates, the exchange rate between the IBT and its underlying asset improves, increasing the token’s intrinsic value rather than its supply. ERC-4626 provides a standardized interface that aligns naturally with this non-rebasing model, where value accrues through changes in exchange rates rather than token quantity.

The role of ERC-4626 in Spectra

ERC-4626 serves as a standardized framework for tokenized vaults, defining uniform methods for depositing, withdrawing, and accounting for yield-bearing assets. It simplifies the representation of yield accrual, especially for non-rebasing tokens that depend on exchange-rate adjustments.

This standard promotes broad composability across DeFi protocols. Vaults or IBTs adhering to ERC-4626 can integrate seamlessly into various ecosystems without needing custom adapters. For Spectra, this means easier incorporation of diverse yield sources, reduced development overhead, and enhanced connectivity within the DeFi landscape.

At its core, ERC-4626 specifies standardized methods for converting between underlying assets and proportional "shares," streamlining integration efforts and facilitating accurate yield tokenization. Non-rebasing IBTs align with this shares-based model, enabling Spectra to interact efficiently with various yield-bearing tokens.

Although optimized for non-rebasing tokens, ERC-4626 can also accommodate rebasing assets through wrapper contracts. These wrappers stabilize the rebasing behavior by presenting a non-rebasing interface, preserving the benefits of the ERC-4626 standard while allowing integration with minimal complexity.

In the case of Spectra, the Spectra4626Wrapper contract wraps rebasing tokens to make them compatible with Spectra’s ERC-4626-based vault framework. It primarily ensures that rebasing tokens can function seamlessly within the Spectra ecosystem itself, translating the rebasing mechanics into a share-based model that aligns with Spectra’s existing infrastructure.

ERC-4626 offers a transparent, standardized approach to representing yield-bearing tokens. Its natural alignment with non-rebasing IBTs and adaptability for rebasing tokens ensures that protocols like Spectra benefit from consistent interfaces, enhanced composability, and straightforward access to a growing range of on-chain yield opportunities.

What are the real-world use cases and applications of Spectra?

Fixed-rate lending and savings

Spectra enables DeFi participants to lock in relatively predictable returns, like purchasing zero-coupon bonds or using fixed-term savings accounts. By separating principal and yield, PTs reduce uncertainty about future APYs and provide a targeted redemption amount at maturity. Note: if the IBT encounters issues—such as bad debt or protocol insolvency—Spectra mechanisms may adjust the final redemption ratio to protect overall protocol health.

We can use Charlie's play for predictable stablecoin returns as an example:

Charlie desires a fixed return on stablecoins for budgeting purposes. He purchases PT-aUSDC at a 20% fixed APY over 180 days. Investing $1,000 yields $1,100 at maturity, irrespective of market volatility. This predictable growth mirrors traditional fixed-income products, supporting long-term financial planning.

Yield leverage and speculation

Spectra’s YTs transform yield into a tradable asset class. By decoupling yield from the principal, traders can independently speculate on interest rate movements, taking advantage of rate volatility without affecting their principal exposure. We can use David's rate bet as an example:

David expects the live IBT APY—the annualized rate of yield accrual when holding the YT tokens—on aUSDC to increase from 8% to around 16%. He purchases YT tokens at an implied 8% APY. If the live IBT APY increases quickly, David’s YT tokens gain value substantially, yielding a notable profit due to the increased demand for YT tokens. Conversely, when the implied APY rate declines, he may face some loss if he sells at that implied APY; however, he can still hold the YT tokens and continue accruing yield at the native rate of aUSDC. If the total yield accrued exceeds his initial investment, he will still come out ahead.

Note that if the implied APY doubles a day before maturity, David’s initial YT investment doesn't double because he has already accrued some yield during the holding period. Only the value of the remaining yield would be doubled in that scenario.

Better upfront yield scenarios

In this scenario, a user sells future yield to obtain immediate liquidity while retaining the principal. Although this approach sacrifices any additional interest that would have accrued, the underlying asset remains intact and can be redeemed at maturity. Note that this strategy is intended for more advanced users.

Example:

- Alice holds liquid staked ETH (like Lido’s stETH). Rather than selling her asset exposure when she needs immediate cash, she splits it into PTs and YTs. Alice then sells the YTs for immediate liquidity while holding the PTs. At maturity, she redeems her PTs for the underlying liquid staked ETH—maintaining her long-term position while addressing her short-term funding needs.

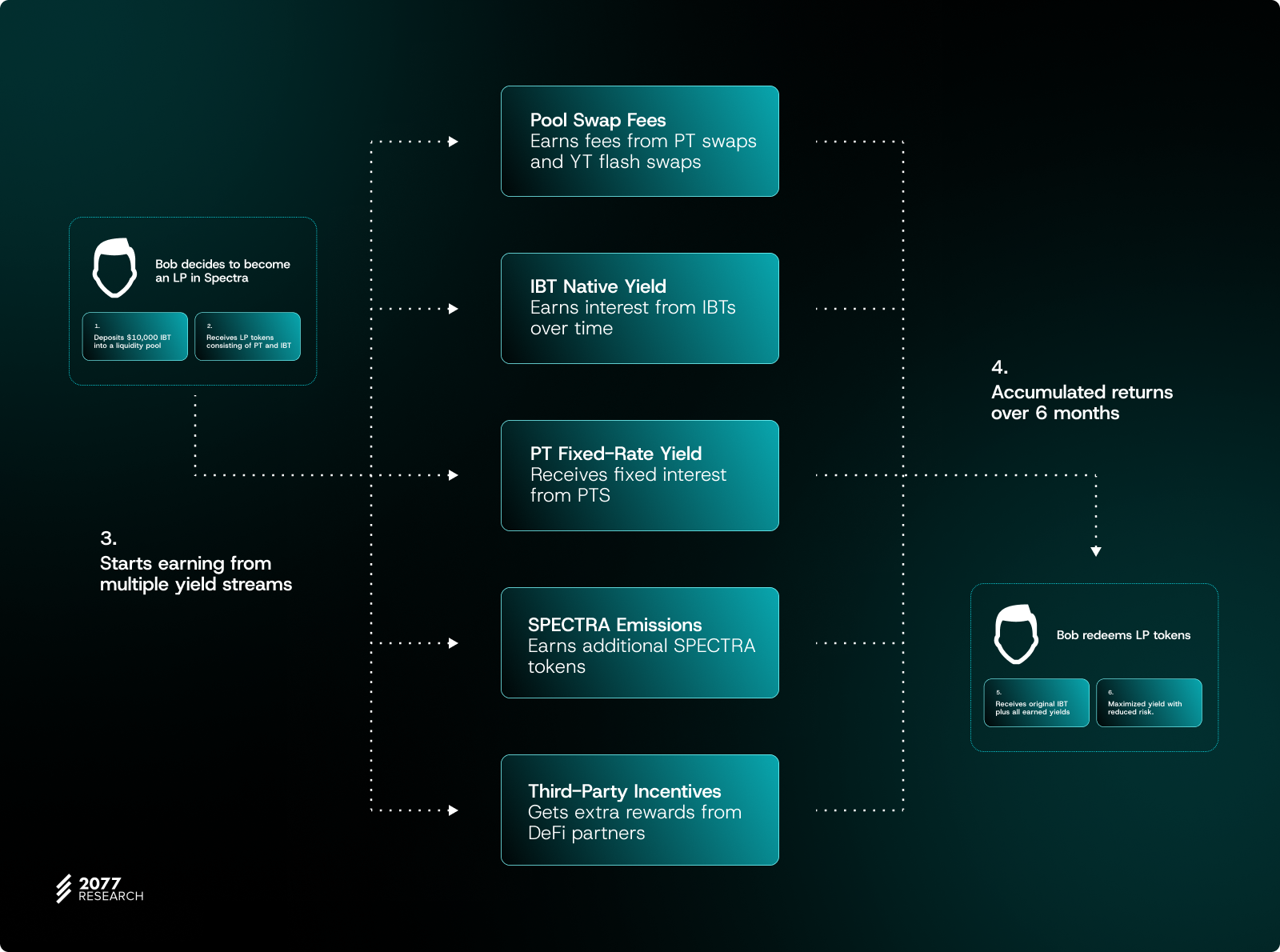

Liquidity provision

Liquidity providers (LPs) in Spectra’s ecosystem benefit from multiple yield streams rather than relying solely on the yield of the raw IBT. By holding LP tokens from Spectra’s pools—composed of PT and IBT—participants can access up to five distinct income channels, broadening their return profile and mitigating risk.

Potential yield streams for LP token holders

- Pool swap fees: LPs earn fees from PT swaps and YT flash swaps, capturing value from all trading activities within the pool.

- The native yield of the IBT: The underlying IBT accrues interest over time. Because an LP token contains a portion of IBTs, holders receive a share of this yield, providing a baseline return.

- Principal token’s fixed-rate yield: Similarly, each pool splits off principal into PTs, which provide a stable, fixed-rate return. Because an LP token also includes PTs, holders gain partial exposure to that fixed rate. As the ratio of PTs to IBTs changes with each trade, the LP token’s APY reflects the prevailing pool composition, effectively combining floating and fixed-rate yields.

- SPECTRA emissions: Spectra incentivizes liquidity provision with SPECTRA tokens, allowing LP token holders to enhance their long-term returns.

- Third-party incentives: External DeFi protocols or partners may add their own incentives, further enriching the total yield potential for LP token holders.

Impermanent loss considerations

Compared to other AMM pools, impermanent loss is marginal throughout its lifespan and non-existent at maturity in Spectra’s pools. This is primarily due to the high correlation between PTs and their underlying IBTs and the stable pricing mechanisms (e.g., Curve) that reduce volatility.

More importantly, since PT holders can claim the underlying IBT at maturity, LPs who wait until maturity face minimal impermanent loss. Over time, this combination of multiple yield sources and reduced impermanent loss risk sets a new standard for liquidity provision in the DeFi space.

While Spectra doesn’t expose LPs to traditional capital loss, the main risk is ending up with a less favorable yield. LPs might find themselves holding lower-yielding assets while having sold off higher-yielding ones to other users. This risk is balanced by earning swap fees from the pool, which helps offset potential yield exposure disadvantages.

Spectra governance and tokenomics

SPECTRA token and governance

On December 17, 2024, the SPECTRA token was introduced, replacing APW as the protocol’s ecosystem token following SIP3. The SPECTRA token inherits many of APW’s governance and utility characteristics but with updated parameters and an expanded maximum supply of 876,751,272 tokens.

Although the APW token remains on-chain (the contract is immutable and cannot be destroyed), APW emissions have ceased, and the token no longer plays an active role in governance. The community-driven migration process allows APW holders to convert their tokens to SPECTRA at a ratio of 1:20. Once migrated, SPECTRA holders gain governance rights within the Spectra protocol. They can also select to lock their tokens as veSPECTRA to boost LP rewards or participate in weekly Gauges.

Key Uses of SPECTRA in the Spectra protocol

- Voting on governance proposals: SPECTRA holders can propose and vote on changes to protocol parameters, contract upgrades, and liquidity incentive structures.

- Enhanced governance participation: SPECTRA can be converted into veSPECTRA by locking it in the vote-escrowed contract. veSPECTRA unlocks additional use cases (discussed in the next section) and is designed to reward long-term commitment over short-term speculation.

The Influence of veSPECTRA on protocol governance

veSPECTRA (vote-escrowed SPECTRA) is a non-transferable token that aligns governance power with a longer lock duration. Inspired by established ve(3,3) and vote-escrow models, veSPECTRA ensures that the most committed participants shape Spectra’s future.

- Time-locked voting power: Users can lock SPECTRA for up to 4 years, receiving veSPECTRA in proportion to the amount locked and the lock duration. Longer lock periods grant a higher share of voting power, ensuring those with sustained interest carry greater influence.

- Governance participation and rewards: veSPECTRA owners receive advanced governance capabilities, such as voting on gauge weights to direct SPECTRA emissions toward specific liquidity pools. Under SIP3, 80% of protocol revenues are distributed to these vote-escrowed SPECTRA holders. However, the SGP6 proposal, currently under review, introduces an updated fee collection and distribution model that may adjust these percentages.

- Dynamic voting power over time: veSPECTRA voting strength decreases as the lock nears expiry. Holders who lock veSPECTRA can extend their lock duration or add more SPECTRA to maintain influence. Once the lock matures, participants can withdraw their original SPECTRA.

Note: Readers should consult the latest documentation or governance proposals for accurate information. Additionally, liquidity providers who hold veSPECTRA earn boosted yields—up to 2.5×—based on their proportional share of veSPECTRA compared to other pool participants. This approach rewards long-term governance participation and encourages deeper liquidity.

Migrating From APW to SPECTRA

Because the APW contract is immutable, the token continues to exist on-chain but no longer has utility within the Spectra governance framework. APW holders can migrate their tokens until December 15, 2025.

- Similarly, veAPW holders can convert their locks to veSPECTRA at 1:10 (reflecting the different maximum lock durations: 2 years for veAPW vs. 4 years for veSPECTRA).

- Migration ensures no dilution in governance power—existing lock durations carry over to veSPECTRA.

After migration, SPECTRA operates on the Base Network, with new contracts managing governance and emissions. APW emissions ended on December 19, 2024, at 02:00 AM CET, effectively capping APW’s functionality.

With these updated tokenomics, Spectra fosters an open, community-driven environment. By aligning incentives around SPECTRA and veSPECTRA, the protocol enables sustainable growth, rewards long-term commitment, and ensures that governance power remains in the hands of its most dedicated participants.

Risk management in Spectra

Participating in IRDs through Spectra involves exposure to various risks, which users should carefully evaluate:

- Smart contract vulnerabilities: Despite audits and ongoing scrutiny, undiscovered bugs or exploits may still occur, potentially affecting user funds or market operations.

- AMM dependency: Spectra relies on external AMMs like Curve. While Curve is well-audited and broadly trusted, unforeseen issues or vulnerabilities are hard to predict and may still arise.

- Counterparty and underlying token risk: Returns depend on the performance and stability of the underlying IBTs. If the issuing protocols encounter instability or other challenges, principal redemption values and yields may be adversely affected.

- Negative yield events: PT holders may receive fewer underlying assets at maturity when the underlying IBT’s share value decreases due to asset depreciation, protocol exploits, or severe market downturns. Although PTs are designed to provide predictable returns under stable or growing conditions, they are not immune to adverse shifts in the underlying yield source.

- PTs value loss: PTs can lose value before maturity due to shifts in IBT rates or market sentiment. For example, Alice acquires 1000 PT-scrvUSD for 950 scrvUSD, expecting a 50 scrvUSD gain at maturity. If interest rates suddenly increase and YT holders capture more yield, the same 1000 PT-scrvUSD might later trade for only 850 scrvUSD on the market. Although holding to maturity guarantees 1000 scrvUSD, selling prematurely could result in a loss.

- Volatile YT prices: YTs reflect future yield expectations. Sudden declines in interest rates can significantly reduce YT values, potentially leading to losses for holders. Users must independently assess and manage these risks.

- Interface and user experience risks:

Front-end interfaces may contain bugs or inaccuracies. Relying solely on displayed information is discouraged; users should verify details from multiple sources.

How does Spectra minimize risk for users?

Spectra employs several measures to mitigate these risks:

- Robust security measures and audits: Spectra’s contracts undergo public audits and continuous community review. Independent security firms and researchers regularly examine the code, enabling proactive fixes and timely updates.

- AMM-agnostic design and governance flexibility: By maintaining AMM independence, Spectra can adapt to changing market conditions and integrate with alternative solutions if existing AMMs face challenges. Governance can swiftly redirect incentives or introduce new sources of liquidity, bolstering the protocol’s resilience.

- Emphasis on due diligence: Users are encouraged to research the protocols and assets underlying their IBTs. Understanding asset stability and track records helps mitigate unforeseen risks. While Spectra provides a robust framework, users must make informed decisions to minimize potential losses.

No DeFi protocol can eliminate all risks, but Spectra’s combination of thorough audits, governance adaptability, transparent communication, and user empowerment aims to foster a more secure and informed environment for IRD participation.

Spectra and the Future of IRDs in DeFi

With DeFi’s continued evolution to incorporate increasingly sophisticated financial products, interest rate derivatives are poised to become essential components of on-chain risk management, predictable returns, and yield optimization strategies. Demand for fixed-rate solutions and advanced yield speculation tools will continue to expand, especially with capital flowing into diverse yield-bearing assets (including RWA-linked tokens).

As RWAs integrate more seamlessly with DeFi, IRDs will transcend the crypto-native sphere and gain relevance in broader financial markets. Spectra’s permissionless architecture, enabling anyone to create markets and manage IRDs, positions the protocol at the forefront of this evolution. By supporting frictionless participation, innovation, and customization, Spectra can redefine how participants price, hedge, and capitalize on interest rate movements.

A key moment in Spectra’s journey is the planned introduction of MetaVaults in Q1 2025. MetaVaults will automate liquidity rollovers and maximize yield, further reinforcing Spectra’s position as a pioneering force in IRD technology and ecosystem development

Technical appendix: Yield token implementation

The core logic ensuring YTs become valueless after maturity is encapsulated in three primary functions: totalSupply(), balanceOf(), and transfer(). These functions override standard ERC-20 methods to enforce protocol rules once the corresponding PT matures.

function totalSupply() public view override(IYieldToken, ERC20Upgradeable) returns (uint256) {

return (block.timestamp < IPrincipalToken(pt).maturity()) ? super.totalSupply() : 0;

}

function balanceOf(

address account

) public view override(IYieldToken, ERC20Upgradeable) returns (uint256) {

return (block.timestamp < IPrincipalToken(pt).maturity()) ? super.balanceOf(account) : 0;

}

function transfer(address to, uint256 amount) public virtual override returns (bool) {

if (block.timestamp >= IPrincipalToken(pt).maturity() && amount != 0) {

revert ERC20InsufficientBalance(msg.sender, 0, amount);

}

IPrincipalToken(pt).beforeYtTransfer(msg.sender, to);

return super.transfer(to, amount);

}Function Details

totalSupply()- Before maturity: Returns the standard ERC-20 total supply, reflecting any remaining YT value.

- After maturity: Returns zero, indicating no yield remains to be claimed.

balanceOf(address account)- Before maturity: Shows the account’s standard token balance (i.e., how many YTs the user holds).

- After maturity: Returns zero, preventing any perceived value in YTs once they no longer accrue yield.

transfer(address to, uint256 amount)- Before maturity: Functions as a normal ERC-20 transfer, allowing YT ownership to move between addresses.

- After maturity: Reverts if a user attempts to transfer a non-zero amount, ensuring that YTs cannot circulate once they have expired.

By enforcing these checks, the Yield Token contract guarantees that YTs will no longer accrue yield and have no transferable value after the Principal Token’s maturity date. This dual mechanism—reverting to zero-value tokens and prohibiting any transfer attempts—maintains protocol integrity and prevents potential misuse, ensuring the yield-bearing lifecycle seamlessly concludes once it matures.

Conclusion

Spectra delivers a permissionless framework for on-chain interest rate derivatives, enabling users to hedge risk, secure fixed returns, and explore yield opportunities with unprecedented flexibility. By standardizing IRD pool creation, embracing composability, and refining the user experience, Spectra provides practical solutions that were previously difficult to achieve in DeFi.

As DeFi matures and incorporates RWAs, interest rate derivatives will evolve from niche instruments into foundational pillars of decentralized financial infrastructure. Spectra’s transparent governance, scalable architecture, and strategic integrations position it to play a central role in this transformation. With Spectra, IRDs become more accessible, intuitive, and essential, driving DeFi toward a stable, efficient, and globally interconnected financial ecosystem.

Disclaimer: The content provided by 2077 Research is for informational purposes only and does not constitute financial, legal, or tax advice. The views expressed are those of the authors and do not necessarily reflect the opinions of 2077 Research or its affiliates. Readers should conduct their own research and exercise independent judgment when interpreting the information presented.