Flatcoins: The Stablecoins With Their Own Price

Explore flatcoins, an innovative alternative to stablecoins, using on-chain mechanisms to reduce volatility without relying on fiat currencies.

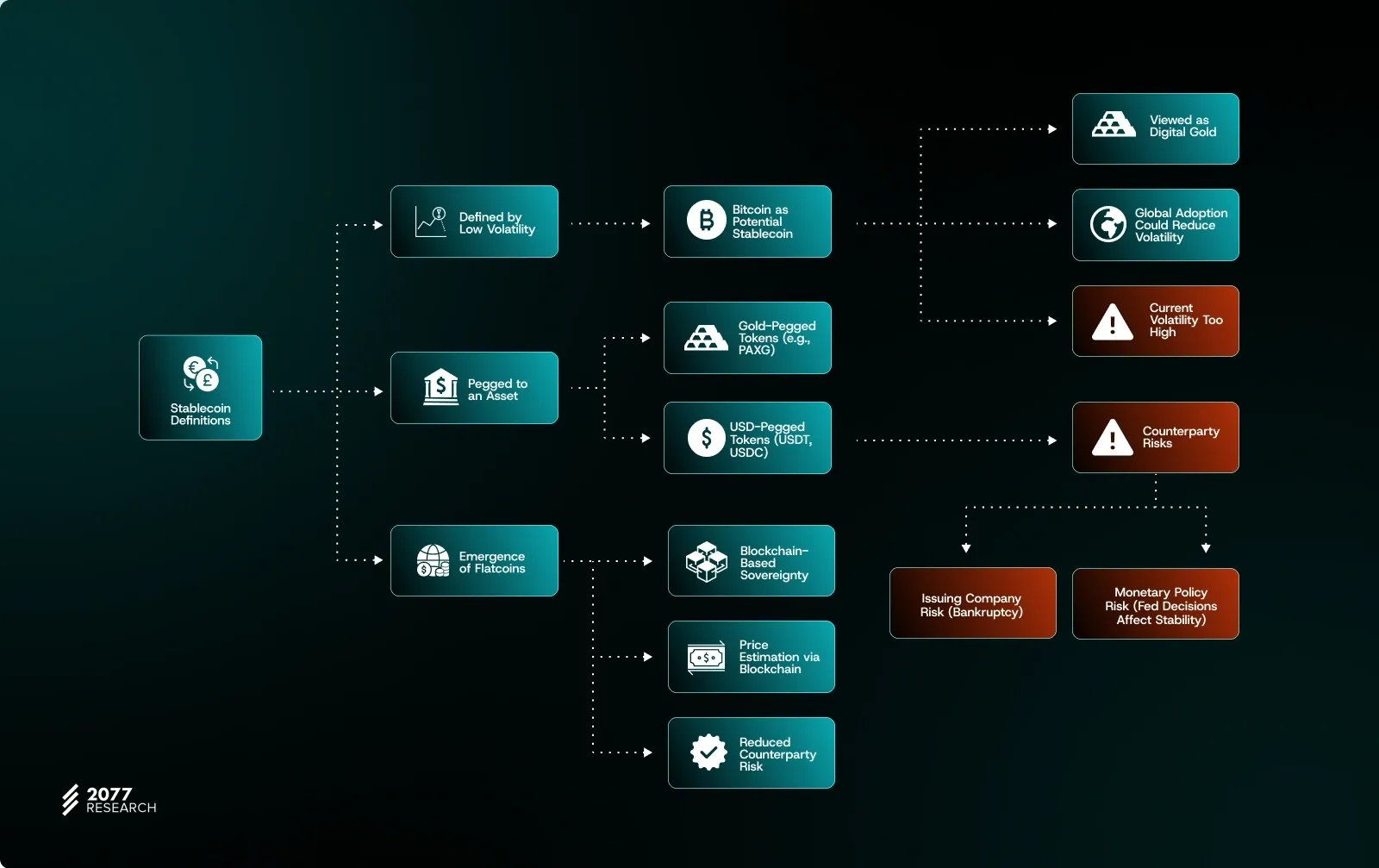

Stablecoins have become a core element of the crypto ecosystem, typically pegged to the US dollar. While they are designed to offer stability in a volatile market, stability in stablecoins is more complex than it cursorily appears. It can be interpreted as a peg to an existing asset, like the dollar, or as an absence of volatility. This article briefly explores the evolving concept of stablecoins and their limitations and delves deep into the emergence of flatcoins or cryptocurrencies that operate independently of traditional currency pegs. We’ll dive into how these novel assets aim to reduce volatility and provide a more decentralized alternative to traditional financial systems.

An introduction to stablecoins

When we think of stablecoins, we generally think of USDT, USDC, DAI, etc. In short, crypto assets pegged to existing currencies. More than 99.9% of traded stablecoins are pegged to the dollar. So, it is safe to conclude that stablecoins are "synthetic replicas of the US dollar."

However, the more we dig into stablecoins, the more complex the notion of stablecoin becomes. We are looking for “stable” assets, but "stable" is subject to many interpretations.

Stability can be conceived as pegging to an existing asset known as stable, or it can be seen as the absence of volatility. The latter is the more relevant outlook, as we use stablecoins to protect against volatility.

So, let’s ask: How do we define a stablecoin?

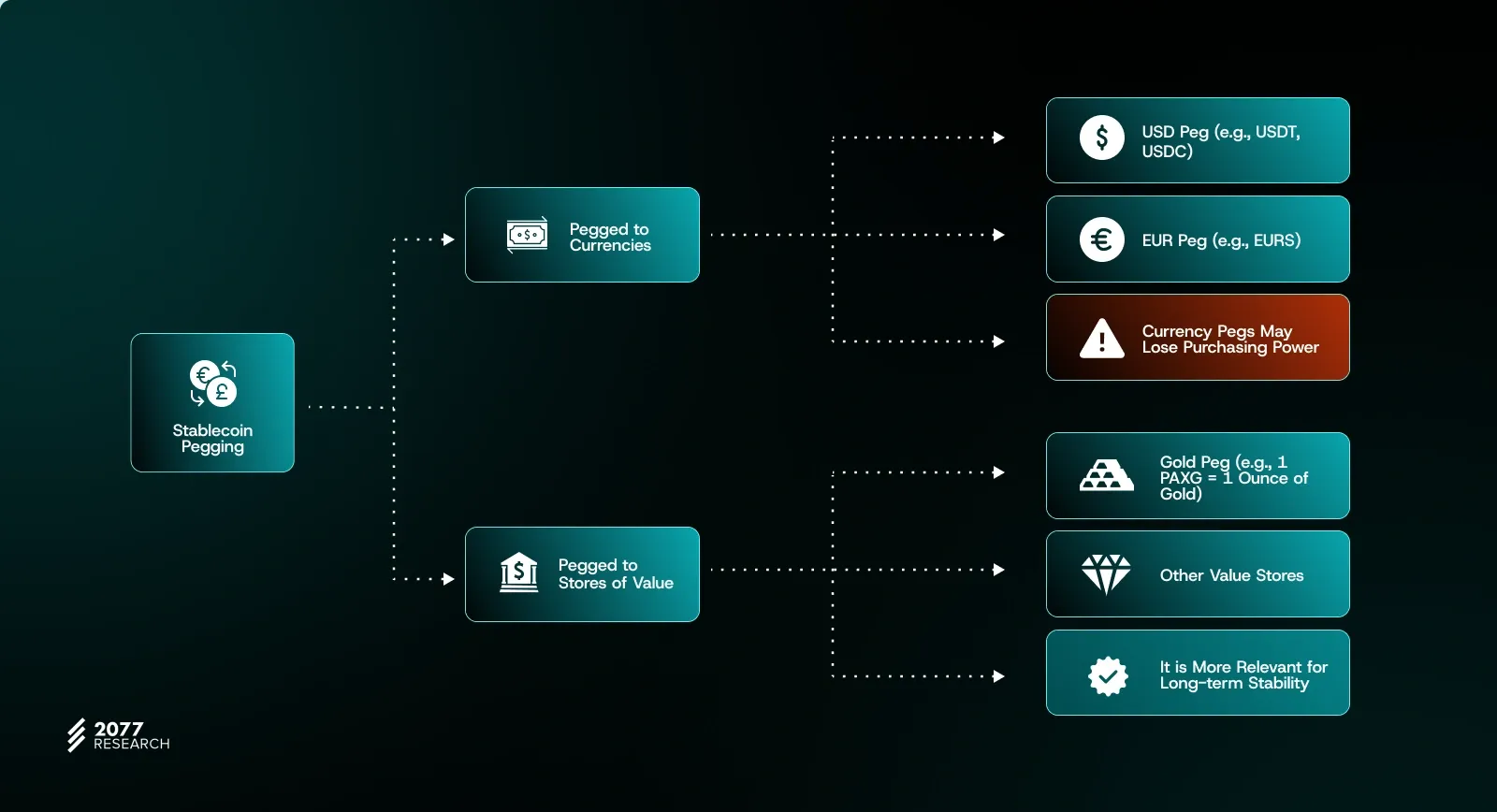

Pegging to a stable asset

From a certain point of view, a stablecoin can be defined by its "peg," meaning the price of the asset it tries to follow.

According to this definition, all assets pegged to existing currencies, such as the dollar and euro, are stablecoins. The problem is that this definition doesn’t work everywhere:

- Between 2021 and 2024, the Turkish Lira lost about 70% of its value against the US dollar, largely due to unconventional monetary policies and high inflation.

- The Lebanese Pound (Lira) collapsed amid the country's economic crisis, losing over 98% of its value since 2019.

- The Argentine Peso experienced severe devaluation, with annual inflation reaching over 200% by late 2023

Indeed, it's not sensible to label a currency as "stable" when it makes us lose purchasing power each year.

A more relevant alternative is to peg the assets to stores of values, for example, with gold like the PAXG from Paxos. Paxos tokenizes physical gold, creates a stablecoin, and allows users to get exposure to gold on the blockchain, given that the value of 1 PAXG = 1 gold ounce.

Absence of volatility

Defining a stablecoin by its underlying asset doesn't make things easier. We could consider another hypothesis: defining a stablecoin by not being volatile. If an asset's price evolution is sufficiently stable over time (or sufficiently non-volatile, take your pick), then absolutely any asset could become a stablecoin.

There exists a scenario where Bitcoin could become a stablecoin. This sentence looks odd, but it can make sense:

- Bitcoin is seen as “digital gold,” so it’s viewed as a store of value, which is a good protection against volatility.

- A global adoption of Bitcoin could cause its volatility to decrease dramatically.

We are far away from this scenario, as the price variations of Bitcoin are still too important. Still, the main idea is to create assets with sufficiently low volatility to stabilize the markets.

However, one problem persists: stability is mostly brought by US Dollar-pegged tokens (USDT and USDC created by Tether and Circle, respectively), and this implies two counterparty risks:

The first one is the issuing company. USDT/USDC is worth $1 because their issuing company has chosen for them to have that value. In case of bankruptcy, there is zero guarantee those assets would still be worth $1.

The second one is the monetary policy. Even though USD volatility is very low compared to crypto assets, USD is still dependent on the American economic policy, which makes its price evolve. In case of a bad decision from the Federal Reserve, the US dollar loses its stability, and the approximately 200 billion of USD-pegged stablecoin also suffers from it.

For some DeFi personalities, relying on a currency controlled by other entities implied too many counterparty risks.

Blockchain technology enabled users to recover the sovereignty of funds. Why not create currencies whose sovereignty and price estimation depend directly on the blockchain? This observation led to the creation of “flatcoins”.

The flatcoins

Flatcoins are cryptocurrencies that are not indexed to any existing currency. They are assets that follow their own course, with smart contracts governing every aspect of the currency, including issuance, monetary policy, etc.

To estimate the price of BTC, ETH, or any other cryptocurrency, we need an intermediary measure:

- It can be hosted off-chain on a peer-to-peer exchange at a price agreed upon by all parties involved, just like the two pizzas paid for with 10,000 BTC on May 22, 2010.

- It can be an oracle, which aggregates off-chain and onchain data, then proposes a weighted price based on data collected upstream.

- It can be onchain, with algorithms defining an asset price depending on onchain supply and demand. Automated Market Makers, such as x*y=k for Uniswap and Stableswap from Curve, could serve the needs of decentralized exchanges (DEXes)

In the case of flatcoins, the price is also determined onchain, and these coins, have their features, like PI controller for Reflexer Labs or reserve-backed stablecoins for f(x) Protocol that we will study.

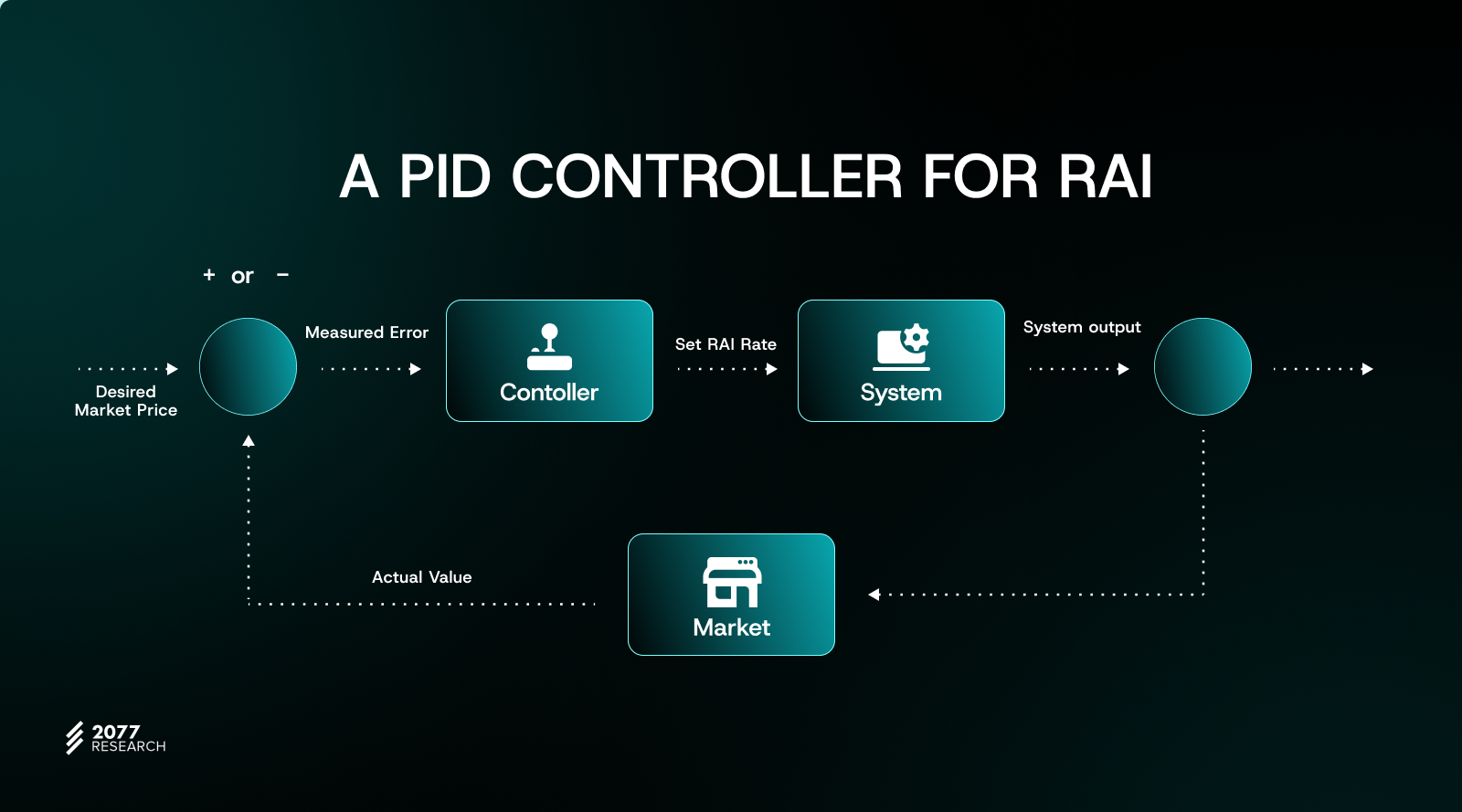

Reflexer Labs (RAI)

The first experiment in this field is the RAI flat coin, developed by the Reflexer Labs team. Currently, one RAI is worth about $3. Minting RAI works the same way Sky/MakerDAO mints stablecoins. It is a classic Lombard loan system in which you deposit ETH as collateral to borrow RAI. If your collateral's value falls below a certain threshold, it is liquidated.

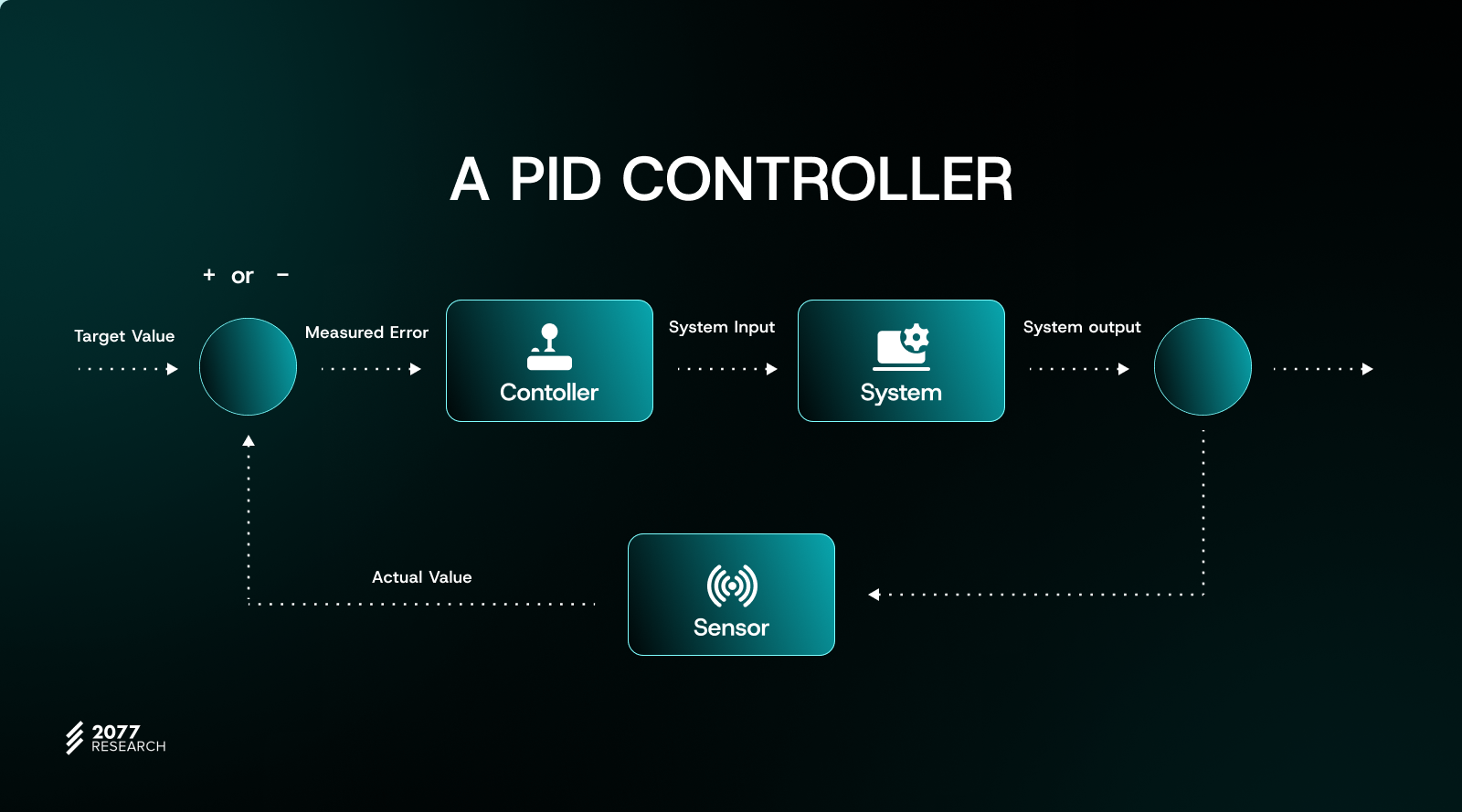

That said, we have one major difference between Reflexer.finance and MakerDAO: Reflexer uses a PID controller.

The chart below shows how a PID controller works:

A PID controller is a system monitoring two values at once: the target value (the one desired by users) and the actual value in the system. Then, it takes the difference between those two values and acts on a specific parameter to converge the actual value with the target value.

Take the example of a car's cruise control, which is a version of a PID controller. Its speed regulator monitors two values:

- The current vehicle speed.

- The target speed chosen by the driver When the target speed is higher than the current speed, the regulator automatically acts on the accelerator to increase the speed. Otherwise, the regulator automatically acts on the brakes to slow down.

Reflexer Labs got inspiration from the PI Controller system, which they repurposed to manage RAI's price autonomously. Note that the “D” in PID is unnecessary as the system doesn’t need a quick reset, and we want to avoid potential oscillations in the asset price.

Just like the example mentioned above, the protocol monitors two values:

- The redemption price, which is the value of one RAI according to the protocol

- The market price, which is the value at which users swap their RAI.

The protocol uses the redemption rate to converge the two values whenever they drift apart. This tool allows the RAI to retrace its path to a balance between supply and demand every time there is an above-normal drift between the redemption and the market price.

If the market price is greater than the redemption price, Reflexer.finance applies a negative redemption rate, resulting in a gradual decrease in the value of RAI over time. For instance, a 10% drop in a year means that 1 RAI will slip from $3 to $2.70.

This mechanism incentivizes RAI holders to sell their holdings since they know the value of their holdings will decrease. On the other hand, RAI minters see their debt becoming cheaper, encouraging them to mint and sell RAI.

The phenomenon reverses if the redemption price is greater than the market price: The redemption rate is positive, and RAI value will increase over time, so RAI minters will see their debt increase as well (unless they pay back their RAI and reduce the supply), whereas users are encouraged to buy RAI.

In a nutshell, RAI introduced its version of interest rate to reach stability:

- When rates are negative, RAI holders pay RAI borrowers

- When rates are positive, RAI borrowers pay RAI holders

The system can keep RAI stable in both underpeg and overpeg scenarios. Let’s see how it does in practice:

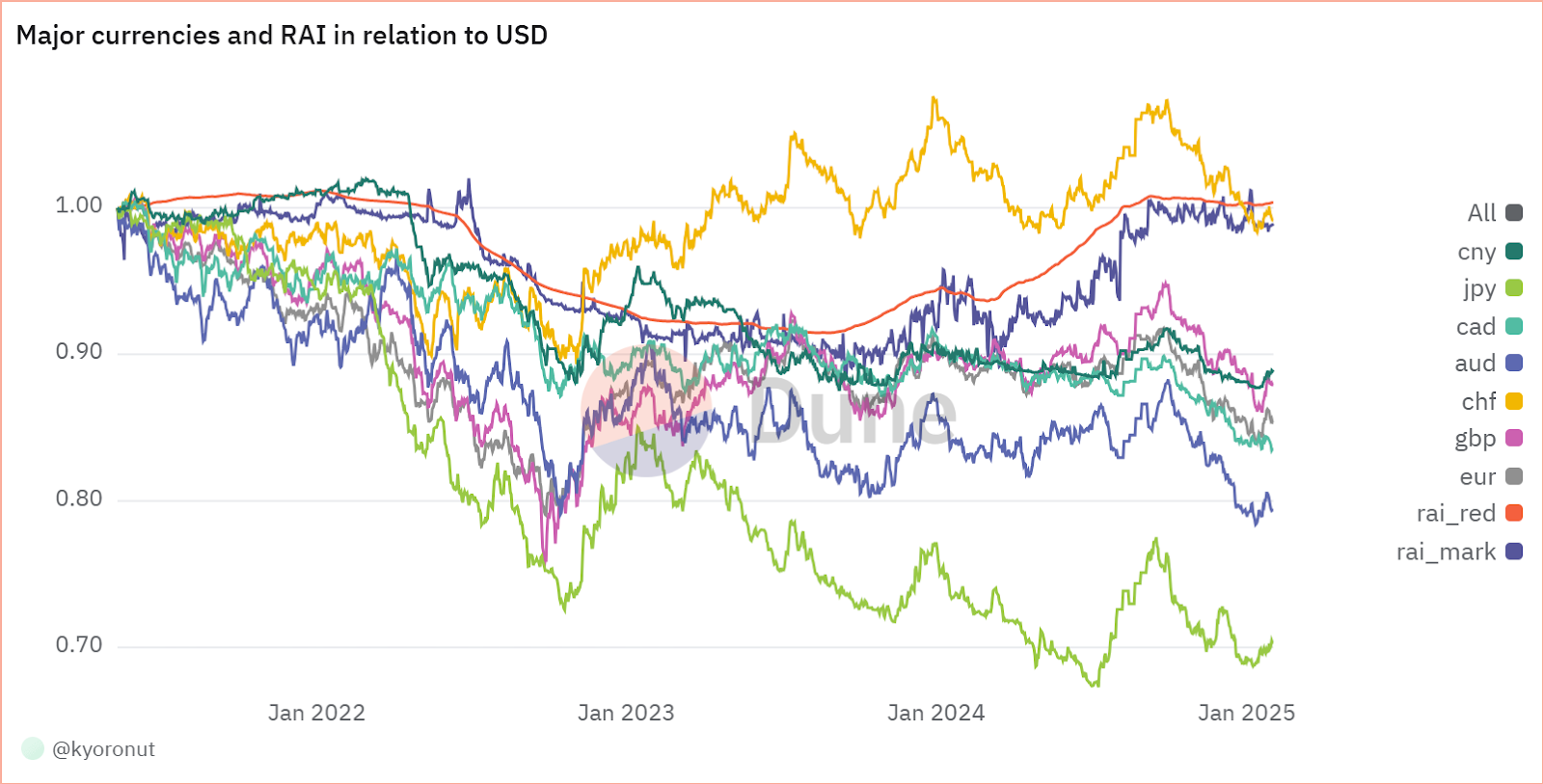

The chart above illustrates major currencies, including RAI against USD. We can draw several conclusions from this:

RAI isn’t perfectly correlated to the USD. Between 2023 and 2024, it lost around 10% of its value against the USD and recently reached a 1:1 ratio.

But in the end, it shows RAI is stable:

- RAI is way less volatile than BTC, ETH, or many other cryptocurrencies

- RAI keeps its value more stable than most existing major currencies. Only CHF surged in value.

If we rely solely on the absence of volatility, then RAI can be defined as a stablecoin.

Letsgethai (HAI)

Letsgethai and its flatcoin HAI is a fork of Reflexer. that was launched on the Optimism network. The key components, such as the PI controller, are the same as RAI. However, there are several tweaks compared to its elder brother:

- HAI is designed to accept multiple collaterals, including Liquid Staking Tokens (LSTs) and volatile tokens like the native token of Optimism OP or Velodrome’s VELO, whereas RAI accepts only ETH.

- Letsgethai has been deployed on Optimism instead of Ethereum, which makes minting and paying flatcoins back considerably cheaper.

- HAI's starting price is $1, a more relatable price evolution compared to USD

The main idea of Letsgethai is to be more accessible to a broader audience.

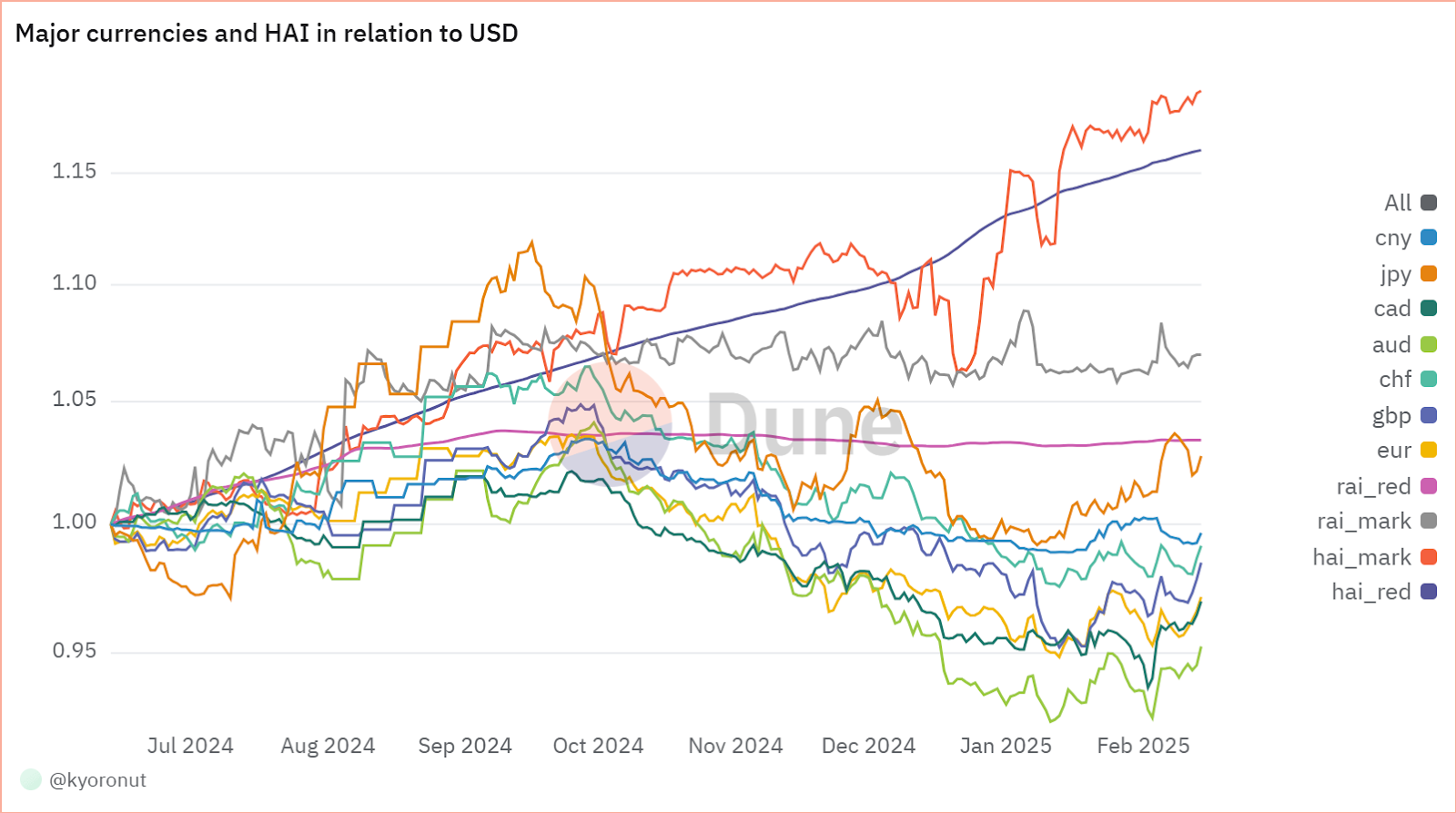

The image above is of another dashboard displaying the price action of major currencies and HAI against USD. and the HAI case is interesting.

Firstly, HAI outperformed every major currency displayed on the dashboard, including USD, with a current market price ranging between $1.14 and $1.15 on pairs with the most volumes.

Secondly, the price increase over time may penalize HAI borrowers as their debt increases, but the main reason for HAI’s price increase is yields and incentives.

Yield comes from yield-bearing assets (wstETH or, more recently, haiVELO) and rewards are in OP and KITE tokens. As long as the yields are superior to the stability fee, HAI borrowers should be fine keeping their positions.

Observing how the price evolves when yields come solely from the collateral used would be interesting.

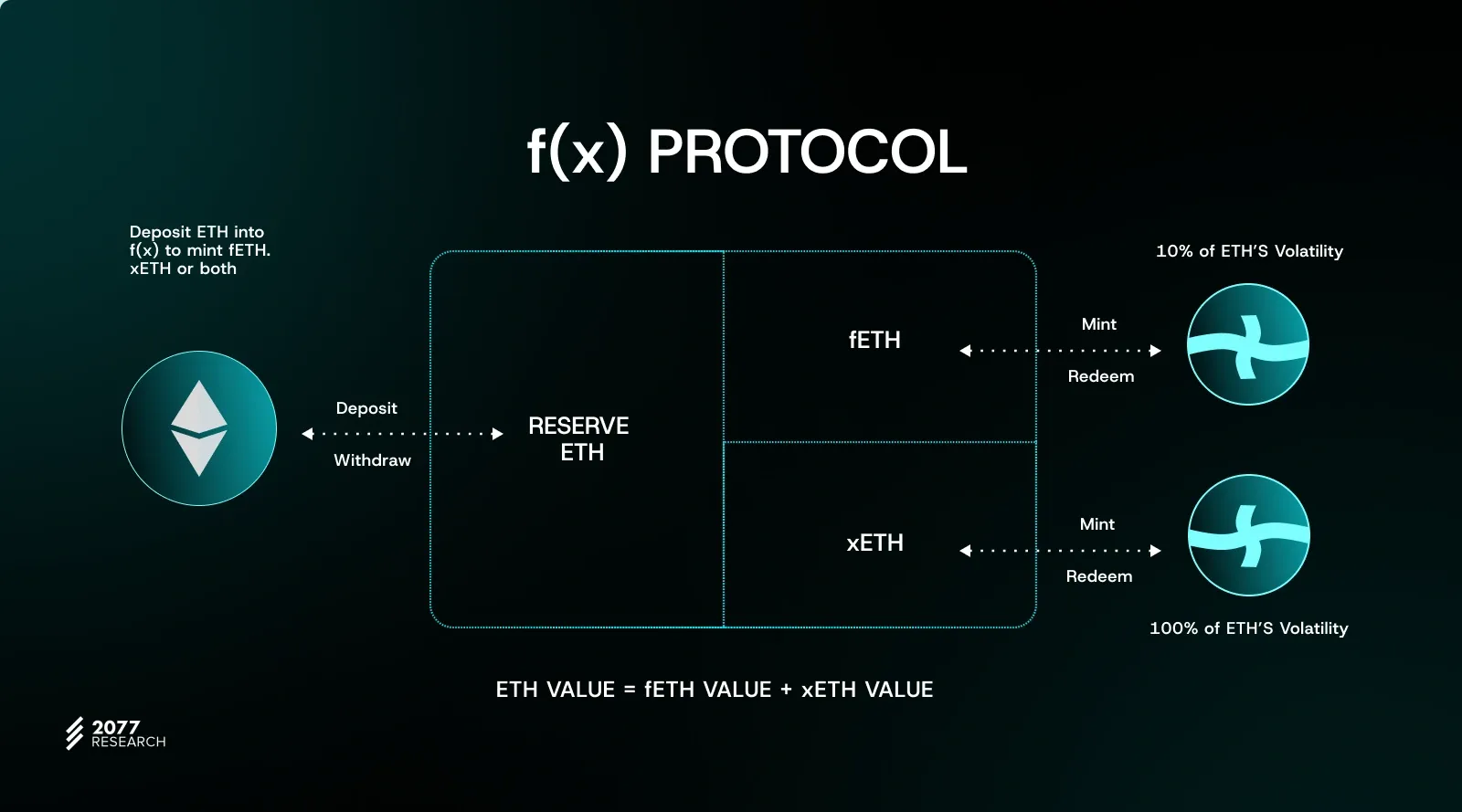

f(x) Protocol (fETH)

f(x) protocol is a quite special but equally interesting case, as it allows users to create "derivative products" of ETH directly with a DeFi protocol. It currently has two versions; the first enables users to mint ETH-backed derivatives, and the second allows users to mint stablecoins and leveraged ETH positions.

This article focuses on the first version, which offers a flatcoin called fETH.

Almost every stablecoin existing via DeFi protocols is minted thanks to collateralized debt positions, meaning that the total supply is the sum of all user’s stablecoin borrowings.

f(x) protocol assets are backed by a reserve: all ETH deposited into the protocol are on the same address, the reserve. A user's ability to borrow assets depends on what they have in this reserve.

When ETH is deposited in f(x), it's possible to create two different types of tokens:

- fETH (Flat Stablecoin): its value is linked to Ether, with volatility capped at 10%

- xETH (Leveraged Stablecoin): its value follows that of Ether, with corresponding volatility

The reserve’s total value always equals the total value of fETH and xETH. If the ETH price increases, the value of fETH is adjusted accordingly, and the remaining reserve value is allocated to xETH. Unfortunately, fETH is not used as much today, as the first version of the f(x) protocol had certain limitations.

To work properly, this model requires a balance between fTOKENs and xTOKENs. If the number of fTOKENs becomes too high, xTOKENs will become extremely volatile and can no longer absorb price fluctuations properly. Conversely, if the number of xTOKENs was too large, their volatility would be too low, considerably reducing the interest in using the f(x) Protocol.

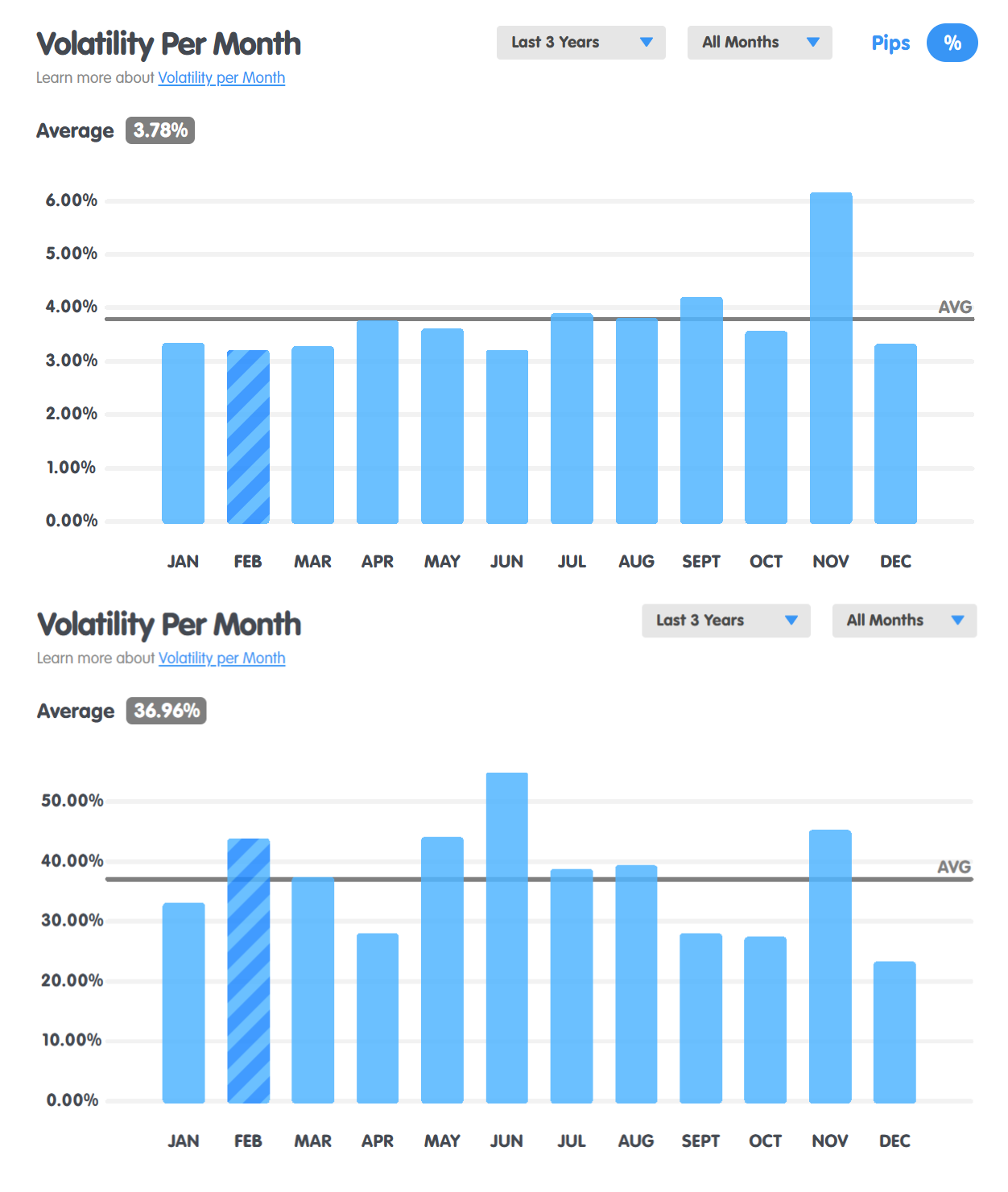

Nevertheless, fETH was an interesting experiment for flatcoins. With 10% of ETH's volatility, fETH had a much more stable price evolution, almost comparable to existing fiat currencies.

To demonstrate an order of magnitude, the euro/dollar volatility is 3.78%/month (over the last 3 years), meaning that each month, the exchange value between euro and dollar changes by an average of 3.85%.

ETH/USD's monthly volatility is 36.9%. However, since fETH replicates only 10% of this volatility, the figure is 3.7%/month, a similar order of magnitude.

fETH has fulfilled its purpose of protecting against volatility, as its numbers are similar to those of the foreign exchange market.

Nowadays, the second version of the f(x) protocol still enables reserve-backed stablecoins, but the stable and volatile tokens have been changed:

- The stable token is USD-pegged

- The volatile token is a leveraged position on ETH, where the user can choose its leverage (currently up to x7).

Challenges and considerations about flatcoins

Like lots of protocols in decentralized finance, flatcoins from issuers like Reflexer finance, Letsgethai, or f(x) Protocol come with technical risks:

- The first risk is that this approach offers debt without collateral. The price of a given collateral can collapse, or the oracle’s price feed can fail. When the platform experiences such an occurrence, the stablecoins advanced to users become bad debt. While the protocol can set up an “insurance fund” to protect against this, too much of it can kill the protocol.

- Protocol exploits are also real vulnerabilities in the case of Reflexer and Letsgethai. The PID controllers they leverage help eliminate the need for an intermediary. However, this introduces the potential for technical risks. Shifts in the market or bugs may manipulate them, leading to fund loss.

A critical challenge for flatcoins is finding their product-market fit between USD-pegged stablecoins (USDC/USDT) and crypto assets like BTC or ETH. Indeed, stablecoins and crypto assets are (involuntarily) the biggest competitors for flatcoins:

- USD-pegged stablecoins and crypto assets have both massive liquidity and a “blue chip” reputation, which flatcoins struggle with.

- Yield-bearing stablecoins are a new trend that contributes to this sector’s growth. Flatcoins have yet to compete at this level.

Considering all the risks involved and the target market, flatcoins are an experiment worth thinking about. However, they are still far from any meaningful adoption.

The Ethereum researcher Dankrad Feist also called RAI “one of the coolest experiments in crypto,” rightly so, as flatcoins raise an important question: “How do we protect our funds from volatility with onchain mechanisms only?” RAI offers a reliable response with its redemption rate. At the time of writing, RAI V2 development is underway.

Conclusion

Flatcoins represent a bold innovation in DeFi that challenges traditional models by relying on smart contracts and on-chain mechanisms to maintain stability. Unlike their dollar-pegged counterparts, flatcoins like RAI and HAI offer a fresh perspective on how digital assets can protect users from volatility without relying on centralized entities or external currencies. However, their adoption faces significant hurdles, including technical risks, regulatory uncertainties, and the challenge of finding a clear product-market fit in the face of established stablecoins and volatile assets. While they may not yet be ready for widespread use, flatcoins offer intriguing possibilities for reshaping the future of digital currency.

The content provided by 2077 Research is for informational purposes only and does not constitute financial, legal, or tax advice. The views expressed are those of the authors and do not necessarily reflect the opinions of 2077 Research or its affiliates. Readers should conduct their own research and exercise independent judgment when interpreting the information presented.