Bringing Permissionless Lending: Making Sense of Euler

Explore how Euler v2 revolutionizes DeFi lending with modular architecture, ERC-4626 vaults, and permissionless customization, enabling tailored lending markets, seamless interoperability, and efficient value capture for diverse assets and users.

The Existence of DeFi Lending

The promise of decentralized lending was to reimagine traditional financial primitives. Yet DeFi’s first wave of protocols opted to sacrifice flexibility for predictability, creating a tension between safety and market development that lies at the heart of onchain credit’s growing pains.

This tension is now reaching a breaking point, while DeFi lending like Compound and Aave have built billion-dollar markets around this premise, yet as the crypto market evolves while traditional yields decline, new dynamics emerge through a fundamental shift in value capture and distribution. The rise of liquid staking derivatives, real-world assets (RWA), institutional demand and even memecoin craze creates an unprecedented need for less “paternalistic” financial lending infrastructure, the idea that sophisticated users inevitably craft complex lending strategies that far outpace the rigid parameters of existing protocols, yet their only path to implementing changes runs through slow, politically-charged governance processes.

While the market has matured, the reality of established DeFi lending faces mounting challenges - rigid frameworks and limited collateral support no longer suffice for today's diverse asset landscape long tail assets. The Fat Protocol thesis back then argued a clear picture: value in crypto would primarily accrue at the protocol layer. It made sense at the time - we all nodded along, thinking about how Bitcoin and Ethereum had massive market caps while applications built on top struggled to capture similar value. But today DeFi lending has thrown a wrench. The reality is messier, more complex, and forces us to rethink everything - most critically, how these systems should be structured in the first place to drive maximum value capture.

The Original Dichotomy: Monolithic vs Modular

Early protocols were recognized as a monolithic paradigm, controlling entire lending stacks - a single unified pool holding major assets, with parameters controlled by centralized governance. This approach represents a decentralized brokers approach to DeFi lending where a defined set of individuals made all key decisions - controlling everything from liquidity provision to risk management.

This model spawned numerous imitators, with Aave, Compound and MakerDAO emerging as dominant players. The approach initially proved successful because it solved two critical problems: bootstrapping liquidity and managing risk in DeFi's early, uncertain days.

As lending transitions to onchain collateral, margins naturally compress due to increased market efficiency. The complexity of monolith isn’t just an operational challenge - it represents a fundamental scaling constraint for DeFi lending. The monolithic model suffers from several structural constraints:

- Risk Contagion: Pooled capital means losses in one asset can affect all lenders

- Reputational Constraints: Every parameter change risks the platform's entire reputation

- Innovation Bottleneck: Conservative governance limits support for long-tail assets, trust assumption much larger than we think

- Capital Inefficiency: Risk parameters must accommodate the lowest common denominator.

The model inherently resists supporting innovative lending products or long-tail assets, regardless of their potential merit, thus pushing the market toward modular solutions or what might be called the free market approach to DeFi lending. But something worth noting, not all modularity is created equal. We're seeing two types emerge:

- Chaos Modularity: Where each protocol has its own governance and fee structure, effectively replacing traditional middlemen with "middle-protocols." Think about trying to build a leveraged position - you're paying fees to lending protocols, DEXs, and various other middleware, each with their own governance making decisions that affect your transaction.

- Cohesive Modularity: Where protocols work together seamlessly while maintaining their independence. Creating systems where primitive protocols provide the foundation, but with abstraction layers that ensure a smooth user experience.

Euler v2 represents this paradigm shift toward cohesive modularity. The lack of flexibility and a competitive marketplace for users to create customized lending pools with tailored parameters has created a gap that they leverage to emerge from the shadows. This transforms lending from a protocol-dominated activity to a market-driven one, where different vault designers compete for capital based on their performance and innovation.

Modularization isn't just architectural - it's a response to the inherent nature of lending as an incomplete contract system requiring human judgment for critical decisions. The result is a new ecosystem where value distributes among specialized players: risk managers like Gauntlet and Re7Capital monetizing their expertise, oracle providers competing for accuracy, and liquidation specialists optimizing for different collateral types.

Yet as markets abhor complexity, we're seeing a rebundling wave through aggregation layers, suggesting that DeFi lending's future lies not in choosing between modular and monolithic approaches, but in understanding which approach best serves specific market niches while maintaining the core promise of trustless, permissionless finance. And nowhere is this story more compelling than in Euler's groundbreaking approach to modularity.

A Glimpse into the State of Euler

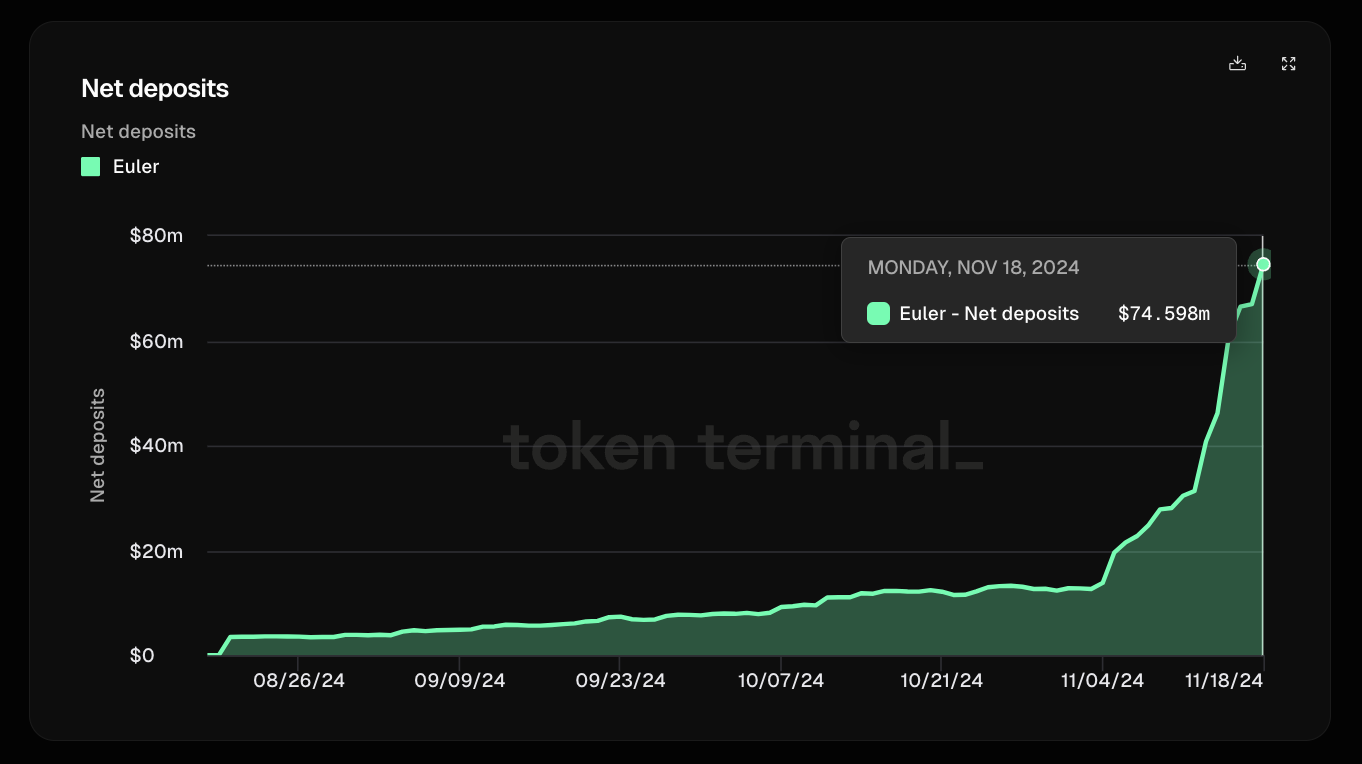

After a rebuilding era and extensive security audits, Euler's relaunch to modularity at core showed an inflection point in early November, catalyzing an aggressive upward trajectory that culminated in $74.59m net deposits, marking approximately a 490% increase in just two weeks (Fig 1).

Fig 1. Euler Net Deposits. Source: Token Terminal

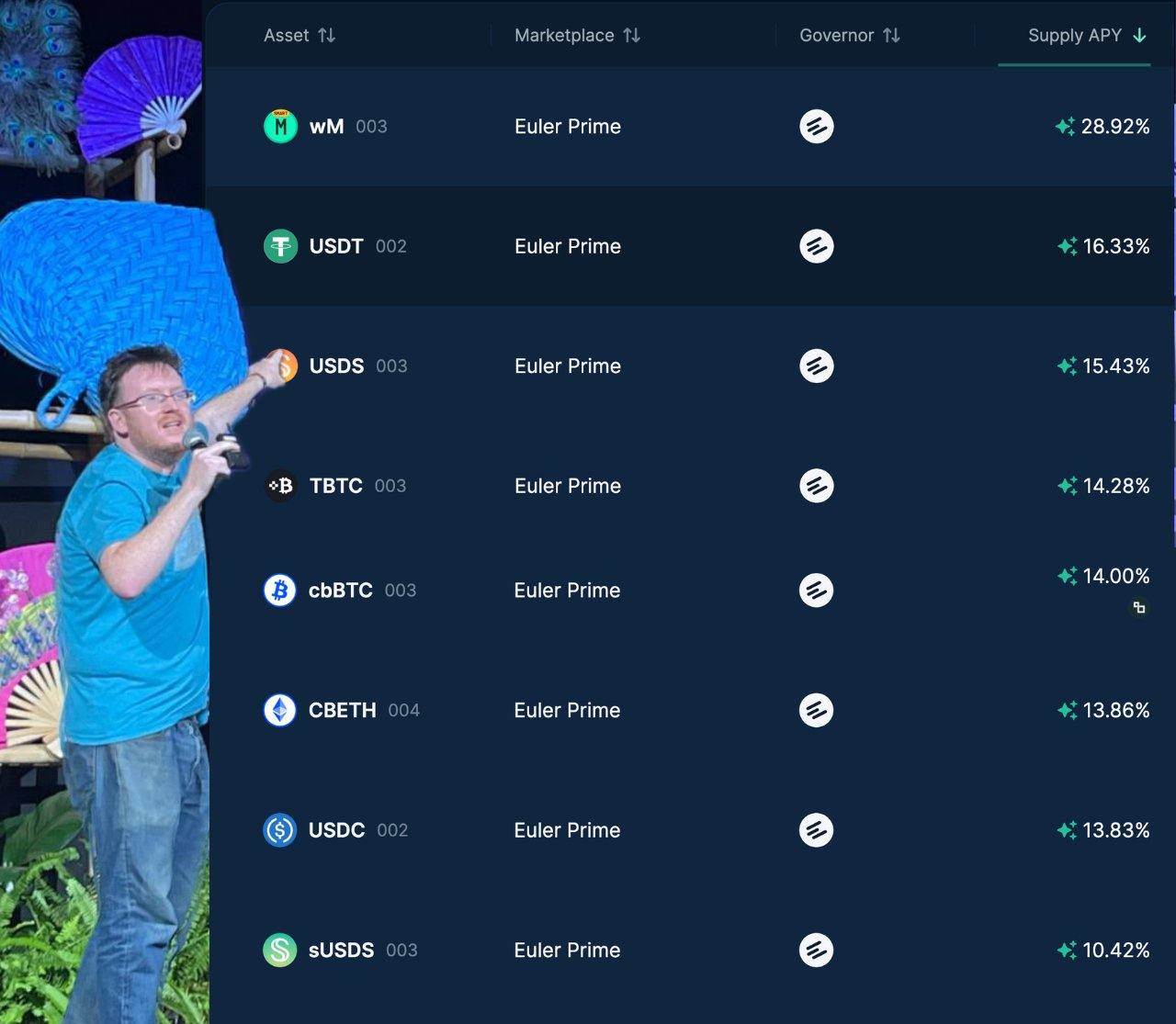

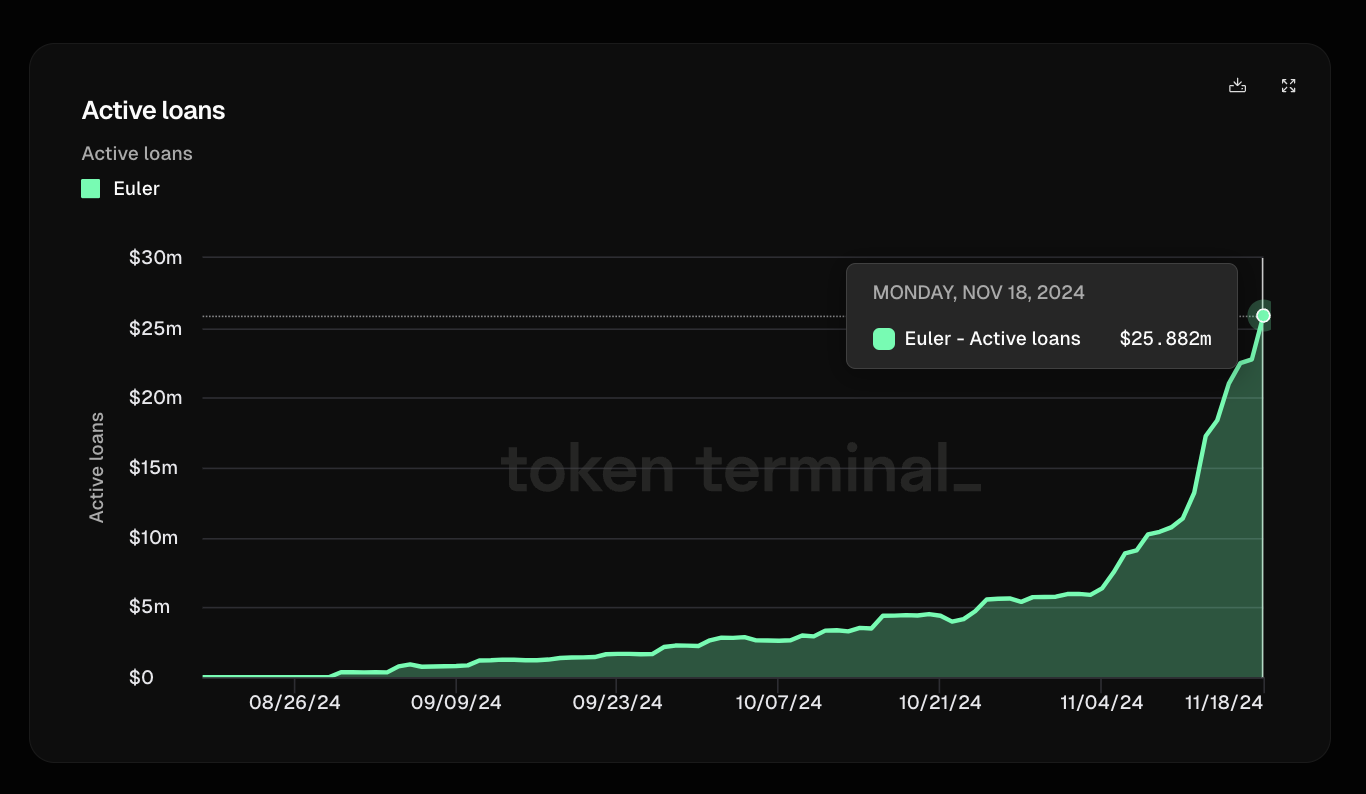

Euler has $25.882m in active loans (Fig 2), with reputable firms like Re7 Labs, MEV Capital, and K3 among potential vault governors. The platform's vault system is positioned to potentially revolutionize capital-efficient, high-yield positions with Pendle PT tokens, offering unique advantages over existing lending solutions.

Fig 2 . Euler Active Loans. Source: Token Terminal

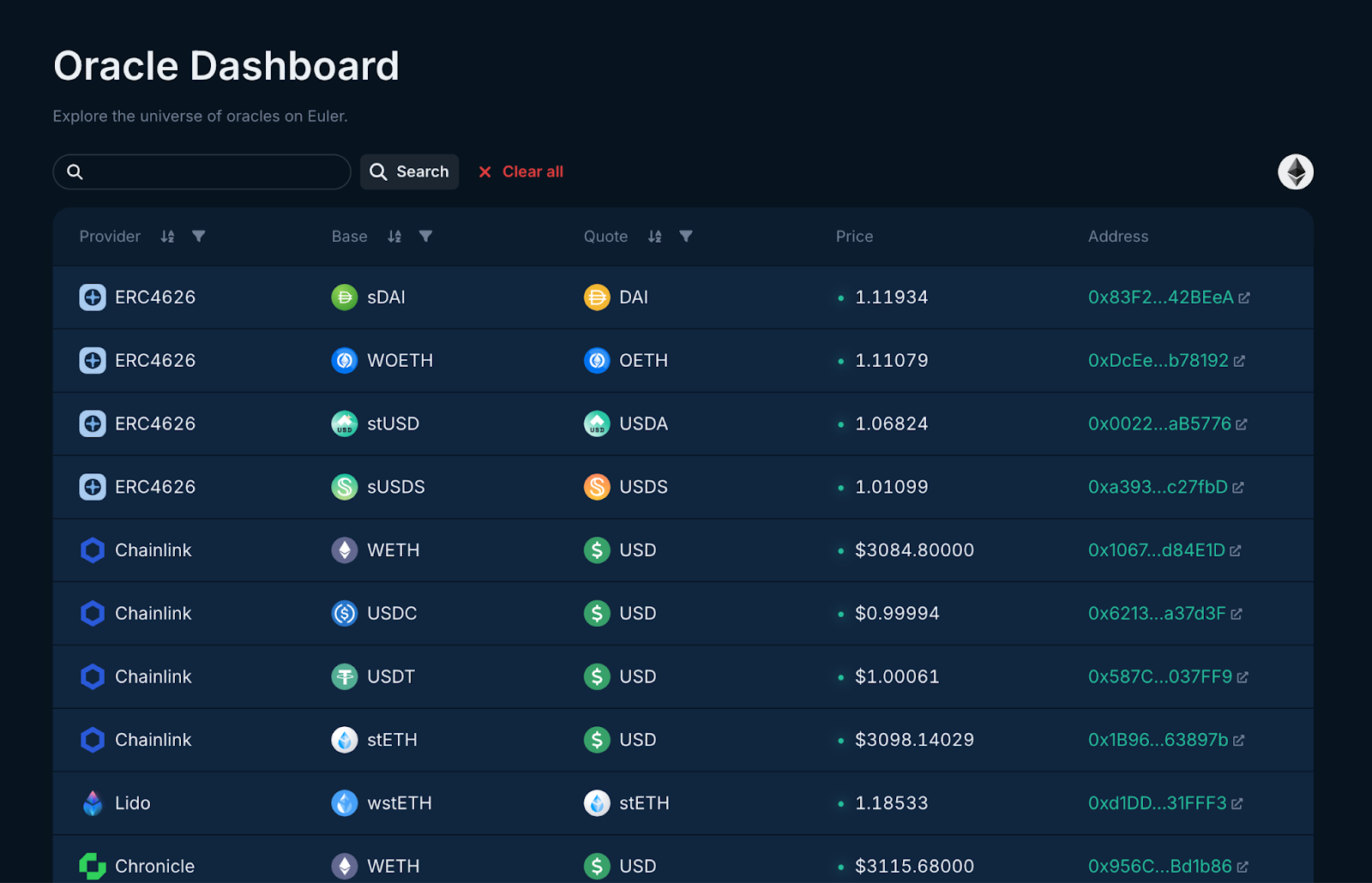

On the technical front, they've developed several crucial public goods: developing the Ethereum Vault Connector (EVC) which lets ERC-4626 vaults serve as collateral (we will discuss this further), helping standardize oracle integration through ERC-7726, and building one of DeFi's most transparent oracle monitoring systems (Fig 3).

Fig 3 . Euler Oracle Dashboard. Source: Euler

Breaking the Monolith: Inside Euler v2's Technical Architecture Foundation

Euler's return to DeFi following its exploit marks more than just a recovery - it represents a fundamental rethinking of lending protocol architecture. Where v1 followed the traditional approach of a single, upgradeable protocol, v2 splits functionality between two primary components: the Ethereum Vault Connector (EVC) and Euler Vault Kit (EVK).

Vaults Everywhere

The EVC and EVK serve as a comprehensive development framework built on ERC-4626. ERC-4626 is an emerging standard for contracts that implement yield-bearing vaults, which will play a crucial role in the future lending market for borrowing and storing collateral. Think of it like ERC-20, the token that we use every day, but designed for yield-generating tokens. Just as ERC-20 standardized tokens and enabled Uniswap to seamlessly integrate any token, ERC-4626 aims to standardize yield-bearing vaults.

The key benefit of the standard is that one integration can work with multiple protocols and applications—write once, use everywhere. There are two main types of vaults in the ERC-4626 context:

- Active Vaults: Traditional vaults where depositors put in funds and the vault actively manages them (reinvesting, seeking yield, etc.)

- Passive Vaults: Vaults that hold funds and wait for borrowers to come and borrow them (similar to Compound's model)

When users deposit into a vault, they receive shares in return. These shares:

- Are ERC-20 compatible tokens

- Don't rebase (amount stays constant)

- As interest accrues, each share is redeemable for a growing quantity of the underlying asset

- Value is determined by exchange rate (total assets/total shares)

The remaining question about this standard is: how do you prevent users from simply withdrawing collateral after taking a borrow? Vaults need to coordinate—they need to work together in some way—and that’s where the EVC comes in.

EVC: Traffic Controller between Vaults

The EVC is an interoperability protocol that enables vault creators to connect their vaults together such that they developers can more efficiently chain vaults together to pass information and interact with one another. The key innovation is its non-invasive approach - it works as a coordination layer without requiring significant modifications to existing systems. This makes it particularly valuable for integrating with both new and existing DeFi protocols.

Core Architecture

- Authentication Layer (EVC): Handles the "who" - verifying identities and permissions of users and contracts interacting with the system

- Authorization Layer (Vaults): Handles the "what" - determining if actions are allowed based on their own rules and states.

This separation makes the system more modular and easier to reason about from a security perspective. For example, when a user attempts to withdraw collateral, the EVC verifies it's actually the user making the request, while the vault determines if the withdrawal would violate any lending terms.

Key Components

Collateral Set

The collateral set is essentially a user's portfolio of vaults they've designated as collateral. Think of it as a list of assets a user is willing to put up as security for loans. Users have full control over managing this set - they can add or remove vaults (when not controlled by a loan), and each vault must be ERC-4626 compatible. This standardization ensures consistent behavior across different types of collateral.

Controller System

The controller system is the heart of EVC's security model. By limiting each account to one controller at a time, it creates clear lines of authority and prevents conflicts. When a user takes out a loan, the lending vault becomes their controller, giving it authority to prevent collateral withdrawals that would make the loan unsafe. This mirrors traditional lending markets where you can't withdraw collateral until you've repaid your loan. The key difference is that this is handled at the protocol level through smart contracts.

Some key features of the EVC include:

- Unified Liquidity and Interoperability: Protocols can accept deposits from other vaults as collateral.

- Standardized Liquidation System: Controllers interact with positions through standard vault functions, reducing attack vectors.

- Flexibility in Asset Properties: The EVC allows for the creation of vaults backed by various asset classes, including NFTs, Real World Assets (RWAs), uncollateralized IOUs, or synthetics.

- Batch Operations: A powerful feature that allows complex operations to be executed atomically, improving gas efficiency and user convenience for position management without requiring traditional techniques like flash loans. Think of it as a sophisticated version of a multi-call transaction, but with added benefits.

- Operators: Users can attach external contracts to act on behalf of a sub-account, unlocking powerful functionality. Unlike controllers, operators can be removed at any time, making them safer for automation tasks. This enables sophisticated trading strategies like stop-losses, take-profit orders, and trailing stops to be implemented as smart contracts that can manage positions automatically.

- Sub-Accounts: Users can create multiple isolated positions meaning positions and risks can be segregated within their single owner account to maintain up to 256 virtual accounts under their main address and easily rebalance collateral/liabilities between them. This is particularly useful for users who want to implement different strategies or manage risks separately.

- Standardized Account Liquidity Checks: Defers liquidity checks and vault status checks, preventing transient violations from causing failures.

- Security Considerations: Vaults must explicitly trust collateral vaults via whitelist; operators require careful vetting.

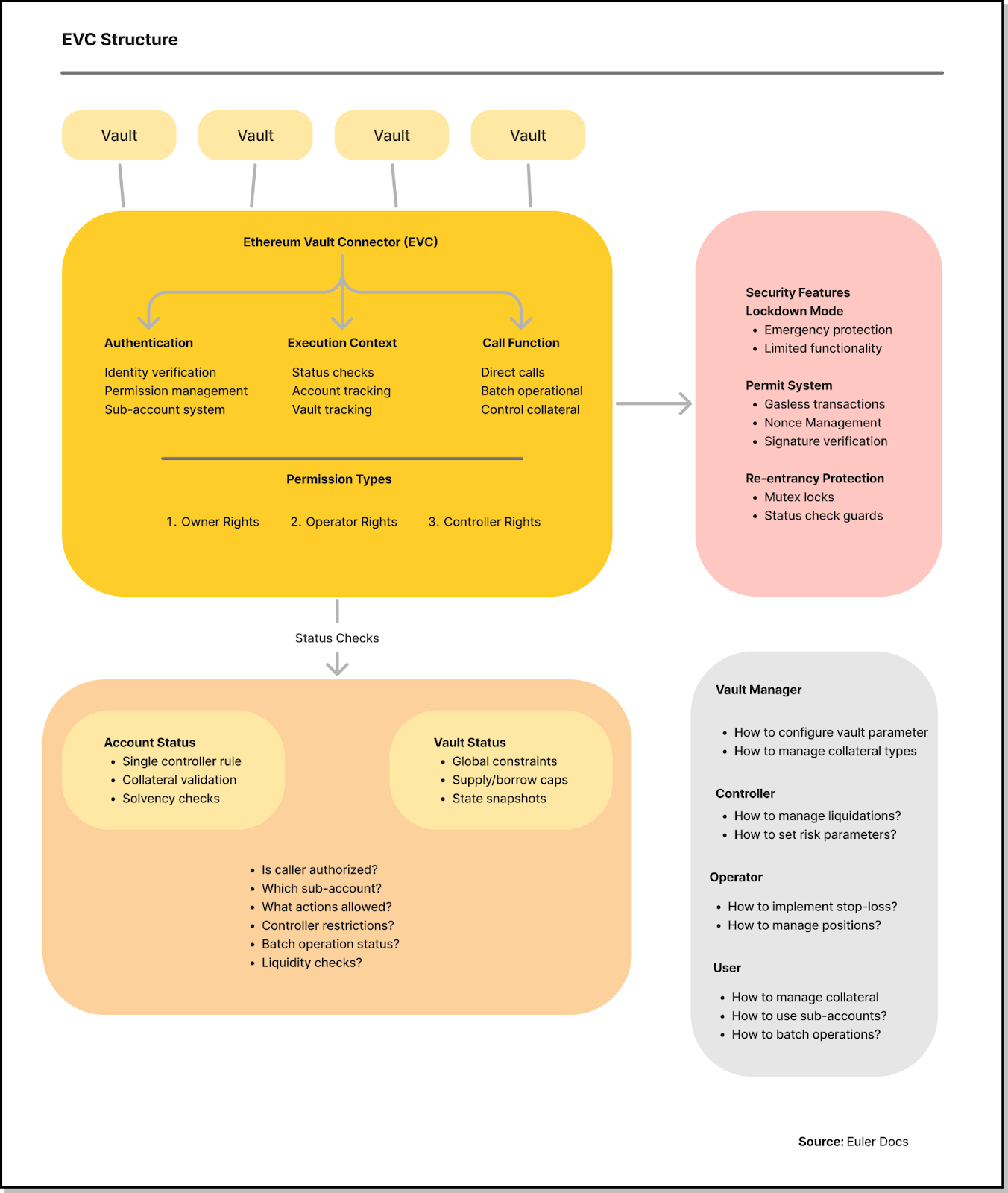

Fig 4 . EVC Structure. Source: Euler Docs

EVK: Vault Creation

In short, the permissionless nature of EVK means to enable users to create their own customized lending vaults; it can be described as a vault development kit that makes it easier to spin up vaults with Euler’s opinionated tech framework. EVK emerges as a sophisticated implementation of this ERC-4626 standard, but goes beyond basic vault functionality.

At deployment, vaults can be created as either upgradeable or immutable through a factory contract, providing flexibility in governance models. The system employs internal balance tracking for gas optimization and implements a virtual deposit mechanism to handle precision and rounding edge cases - critical for assets with varying decimal places. This approach solves historical challenges in lending protocols where precision loss could lead to accounting discrepancies.

Core Architecture

Vault Governance Models

- Managed Vaults

The managed vault system provides flexibility in governance through different control mechanisms. When creating a vault, the deployer becomes the initial governor and can retain this control, ideally through a multisig or governance contract. This model allows for active management of vault parameters and settings, enabling responsive adjustments to market conditions. Multiple vaults can be managed by the same multisig, facilitating cluster-like lending products, or they can be individually controlled for more isolated management.

- Immutable Vaults

At the opposite end of the governance spectrum are immutable vaults, created when the governor address is set to zero. These vaults have fixed configurations that cannot be changed after deployment, providing users with certainty about the vault's behavior. This immutability can be particularly attractive for users who prefer predictable, unchanging protocols.

- Hybrid Governance

Between fully managed and immutable vaults lies a spectrum of hybrid governance strategies. These can be implemented through proxy contracts that limit governance actions to specific functions, such as pausing operations or adjusting LTV ratios. These proxy contracts can include timelock mechanisms and other controls, providing a balance between flexibility and stability.

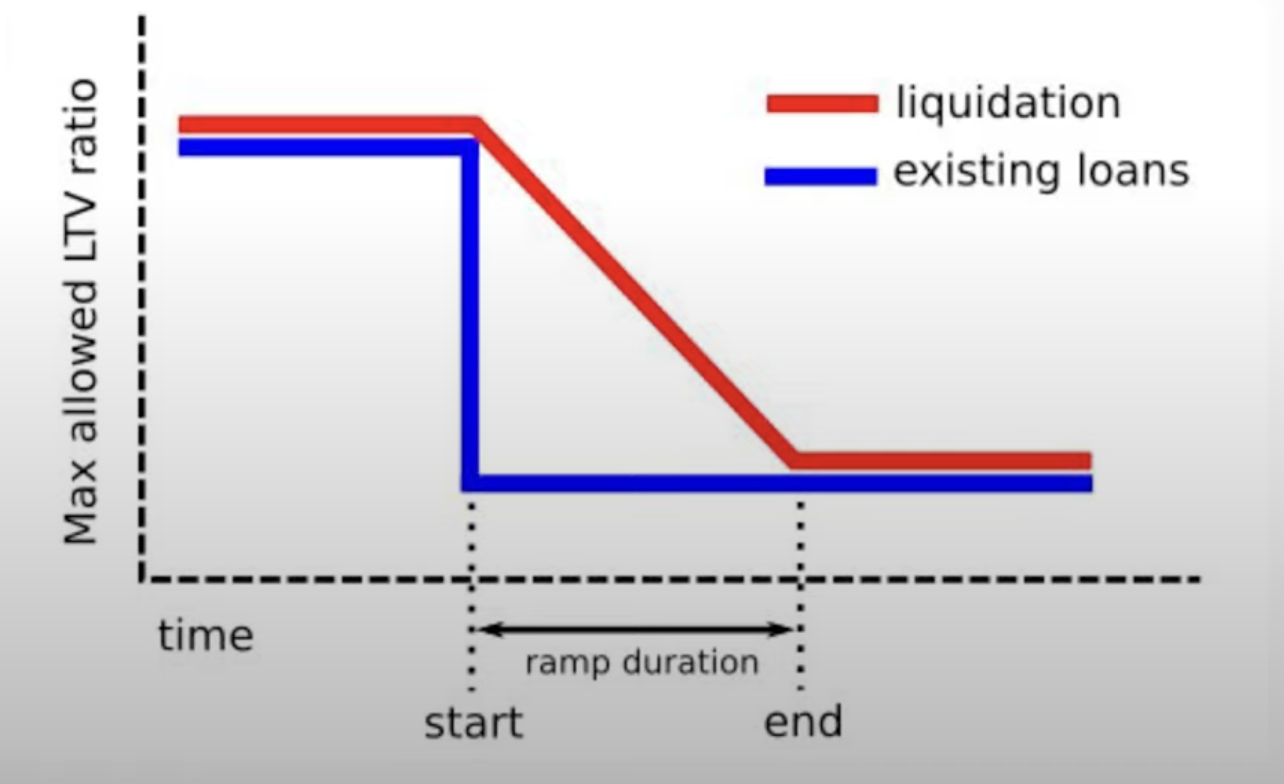

The EVK features a robust security architecture centered on vault share pricing protection. It implements internal balance tracking and virtual deposits to protect against manipulation attempts and pool donation attacks. The system's LTV (Loan-to-Value) ramping mechanism introduces a thoughtful approach to risk management, allowing existing positions to adapt gradually to parameter changes while applying new limits immediately to fresh positions, effectively balancing borrower protection from sudden liquidations while maintaining protocol safety (Fig 5).

Fig 5 . LTV Ramping. Source: Euler Docs

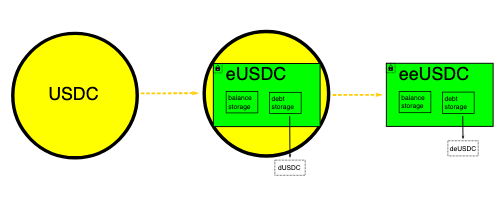

A key innovation is the nested vault system, enabling vault shares to serve as underlying assets for other vaults. This creates a composable architecture where users can stack yields across multiple vault layers - for instance, an eUSDC vault token holder benefits from both eUSDC yields and additional lending returns (Fig 6). This feature particularly helps new lending pools bootstrap liquidity by offering competitive yields from launch. Complementing this is a flexible reward streaming system that enables permissionless liquidity mining programs, capable of rewarding leveraged positions based on their full nominal value rather than just base deposits.

Fig 6 . Nested Vaults. Source: Euler Docs

Rethinking Value Capture in Modular Lending

Fee structure is designed with both flexibility and efficiency in mind:

- Managed Vaults: Governors can set and adjust fee parameters

- Immutable Vaults: Fixed fee structures defined at deployment

- Nested Vaults: Fee considerations for multiple yield layers

- Fee Distribution: Sharing between vault creators and Euler DAO

Here’s where things get interesting, the mechanism behind this system is FeeFlow, an innovative open-source module that revolutionizes how fees are handled and converted. It is agnostic to the underlying protocol it accrues fees from, and can convert fees into kind of token. Unlike the traditional “dump everything in treasury and figure it out later” approach, it introduces a reverse Dutch auction system that solves the asset consolidation problem that has plagued DeFi.

This system periodically auctions accumulated fees by systematically reducing prices, providing a MEV-resistant and efficient path to convert various assets into unified tokens like ETH, stETH, USDC, or potentially EUL, while automatically allocating a portion of generated interest to fees, creating a passive income stream for vault creators and ensuring the Euler DAO receives its share.

The entire system is built on the ERC-4626 standard, ensuring seamless integration with the broader DeFi ecosystem while maintaining backward compatibility with ERC-20 tokens. The implementation uses non-rebasing shares for predictable integrations and employs a sophisticated exchange rate mechanism that considers both actual token balances (cash) and outstanding loans for accurate share pricing. This comprehensive approach, combined with virtual share protection mechanisms, creates a secure and efficient system for managing yielding vaults.

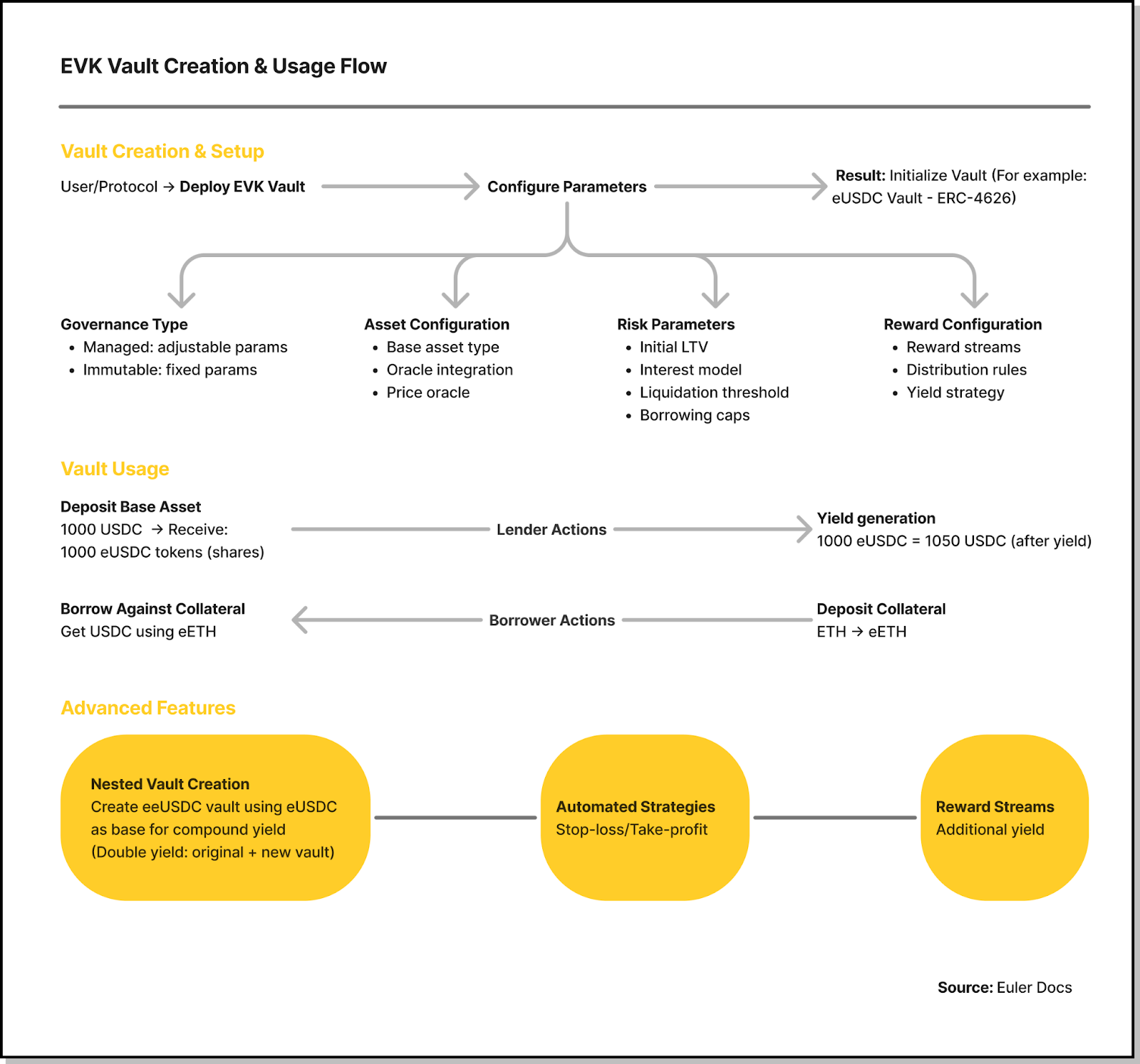

Fig 7 . EVK Vault Creation & Usage Flow. Source: Euler Docs

At the end of this technical discussion, tailor your own risk. Euler uses a modular ecosystem of vaults to give you full flexibility in your lending experience:

- Core: Traditional governed lending (Euler v1)

- Edge: Permissionless lending markets with flexibility of parameters

- Escrow: Support for any ERC20 as collateral, but without yield-generating.

The two technological architectures behind it act as base layer lending infrastructure: the EVC serves as the protocol's connective tissue, orchestrating vault interactions and position management, while the EVK emerges as a sophisticated toolkit for crafting bespoke lending markets. At their core, both components create what could be DeFi's most comprehensive lending framework yet - spanning from traditional DAO-governed markets to cutting-edge permissionless deployments. Euler's architectural approach suggests a future where lending markets aren't just isolated pools, but composable, interoperable building blocks. This vision of lending could fundamentally reshape how we think about capital efficiency in DeFi.

Looking ahead: DeFi as a True Product-Market Fit

DeFi lending, despite its maturity relative to emergent sectors like liquid staking, restaking, high-yield bearing stablecoins and others, stands as one of the few verticals demonstrating genuine product-market fit without succumbing to ponzinomics. This foundation suggests continued innovation is not just possible but probable in upcoming market cycles

However, the true test lies in adoption. While Euler has addressed technical challenges and security concerns, key questions remain:

Product-Market Alignment

- As protocols accumulate increasingly diverse fee streams, how viable is Fee Flow's uncapped token approach when gas optimization becomes critical at scale?

- Does the market need this level of complexity, or will minimalist approach win?

- Who is the true target user: sophisticated traders or lending operators?

Platform Strategy

- Is Euler primarily an infrastructure play or a direct lending platform?

- Without a MetaMorpho equivalent, what's Euler's path to attracting lending operators?

- How critical is the missing "pool manager" abstraction for operator adoption?

Growth Trade-offs

- How will Euler's complex feature set influence market dynamics between Core and Edge segments?

- How does the mechanism balance the trade-off between maximizing auction efficiency and ensuring timely fee conversion?

The DeFi lending landscape is evolving toward market specialization rather than winner-take-all outcomes. While Euler targets sophisticated users with its comprehensive toolkit, success will ultimately hinge on ecosystem development and market-specific optimization. Today's technical superiority must translate into tomorrow's market adoption - a transition that remains the protocol's primary challenge.